Omniwealth’s Property Sale Series starts with the question: When to sell an investment property? The first study looks at paying down home debt.

There are times when you should listen to your parents, and times when you should not listen to your parents.

I have a couple who are clients. When they first got married in their mid-twenties their parents told them: “Get a mortgage, buy a home and pay off the mortgage as fast as possible.” This first home was a small two-bedroom apartment in a 1930’s-built apartment block.

Lots of character but not suitable for them and the extra two children they now have. Two years ago, they moved out to rent a larger home and have been renting out the apartment since. It was good parental advice to listen to. For the home they paid around $500,000 over a decade ago – today it’s worth $1 million. The remaining mortgage is $200,000. That was good parental advice to follow.

They now need a bigger home. Their parents are saying to them: “Buy a new home and keep the apartment for a long-term investment. Why would you sell the apartment? That’s a crazy idea. It’s cash flow positive”

So, this is where good parental advice turns into bad parental advice. I shall tell you why.

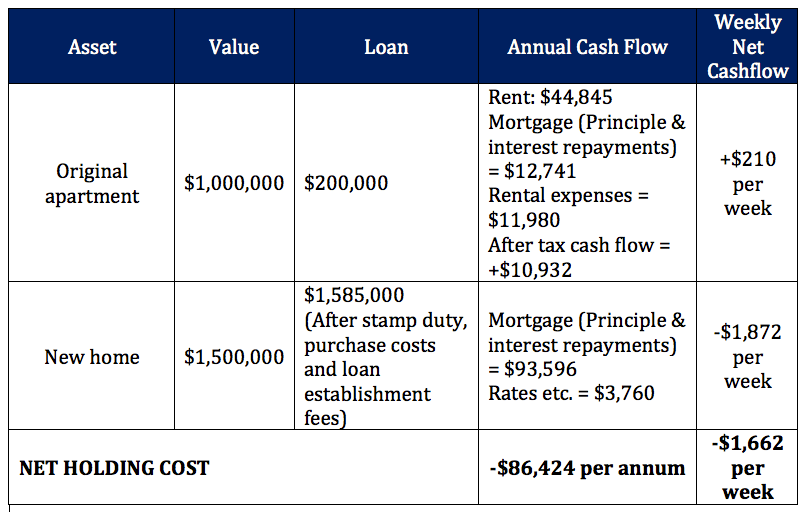

Scenario 1

If they followed parental advice second time around …

If they keep their apartment, their maximum borrowing capacity is around $1.85 million. They can comfortably borrow enough to buy a larger home valued up to $1.5 million plus purchase costs. (Presuming they have not maxed out all of their borrowing capacity.)

So, their situation looks like this:

In this scenario, the original apartment has a lot of equity in it. However, by drawing that equity for the purpose of buying a new home, that new debt is still non-deductible debt even though it may be secured against an investment property.

Having a $1.585 million-dollar home loan at long-term average interest rates of around 7%pa will require a total of $3.796 million in principle & interest loan repayments over 30 years. Our couple will need to have earned around $6.274 million over the 30 years pre-tax to pay off their new home loan. OUCH!

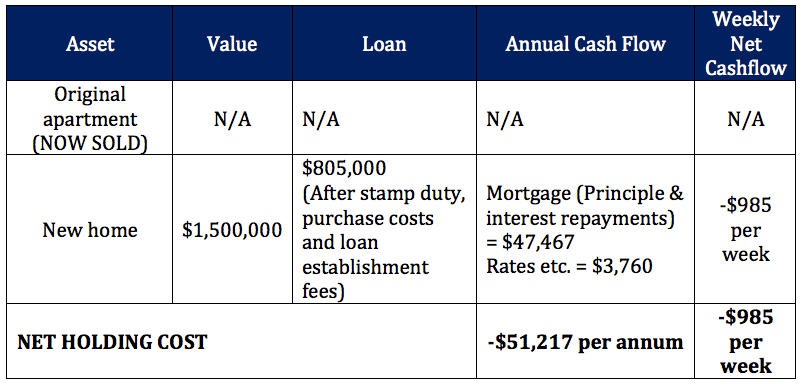

Scenario 2

If they seek proper advice …

Now, let’s be smart. Let’s drop the emotion attached to that beautiful full brick quaint apartment they bought when they first got married (and yes – not following parental advice now).

I have assumed they would clear around $775,000 after agent sales fees and paying off the original mortgage. As this was their original home, and they have been renting for the last two years, the sale of the property is still capital gains tax free (CGT). There is a rule that if you sell a property that was originally your home and you have been renting another property to live in that you do not own, you can sell that property CGT free for a period of up to six-years after moving out.

Let’s look what happens if we use all of the proceeds from the apartment sale towards the new home purchase.

This has created a weekly cash flow saving of $677 per week by not following parental advice the second time around.

By selling the original investment apartment, and reducing the home loan to $805,000, at long-term average interest rates of around 7%pa will require a total of $1.928 million in principle & interest loan repayments over 30 years. Our couple will need to have earned around $3.186 million over the 30 years pre-tax to pay off their new home loan.

This has saved a total of $1.868 million in principle & interest loan repayments over the life of a 30-year loan.

Importantly, they now have plenty of equity in their new home. If suitable, they can draw on this equity to purchase new investment assets. If the new debt secured against the home is used for investment purposes, this will then be tax deductible debt.

This is the first example I will write in a series of when it may be appropriate to sell an investment property. Getting suitable advice has made a big difference to this couple’s weekly cash flow and their future.

Andrew Zbik

Senior Financial Planner

Omniwealth

Tel: (02) 9112 4316

Mob: 0422 038 253

andrew.zbik@omniwealth.com.au

www.omniwealth.com.au