Investment Bonds have benefits and features which are worthwhile evaluating as a way to supplement superannuation or even as an alternative tax-effective vehicle.

1. When super contribution caps are maxed out – selling a property

Anna is 55 years old and is on the highest marginal tax rate of 47% and expects to earn $250,000 p.a.

Anna has recently sold down her investment property with net proceeds of $300,000 received. Her superannuation contribution limits have been capped out but she wants to invest surplus income of $10,000 p.a. for the next 10 years.

She is looking to reinvest her property proceeds and surplus income in a tax effective manner.

Strategy

Anna invests her investment property proceeds of $300,000 into an Austock Imputation Bond and contributes an additional $10,000 each year via a regular savings plan.

Benefit

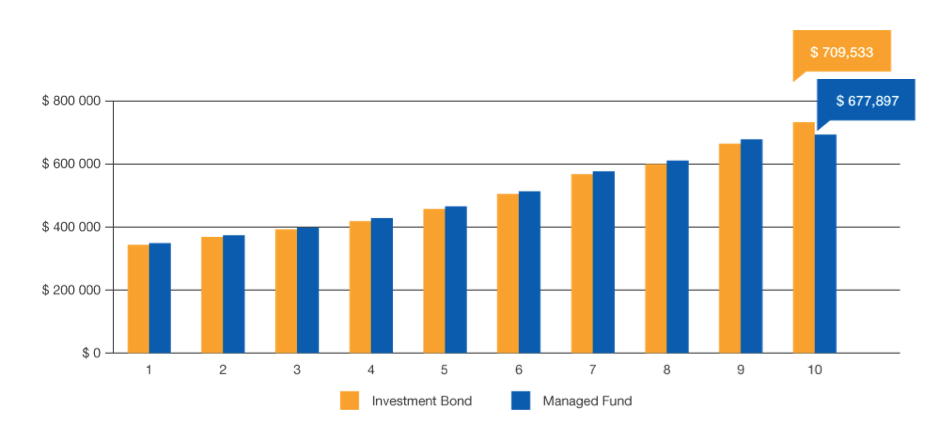

By age 65, Anna will have contributed $400,000 which she would not have been able to contribute into her superannuation because she has reached her contribution limits. Her Investment Bond will have reached a value of $709,533 after 10 years.

By contrast, if she had invested her funds into a managed fund, her accumulated value after tax would have been $677,897.

Anna is also able to access her Investment Bond benefits prior to her intended retirement age if she requires.

End investment balance (after tax) after 10 years*

* Assumed annual return of 9% p.a. net of fees (5% income return, 4% capital growth) with 100% annual turnover and 50% CGT discount.

2. When super contribution caps are maxed out – excess income issues

Susan, a lawyer and husband John, a paediatrician are both in their late forties on very high incomes. Both are on the highest marginal tax rate of 47%.

They easily use up their annual superannuation caps – after salary sacrificing their maximum contributions – they still have a sizable surplus. They currently have $250,000 to invest as a lump sum which they cannot contribute into their superannuation. They also have annual surplus income of $40,000 (combined) which they would like to invest for the long term.

With high lifestyle and household expenses including three children in top private schools – they want a non-superannuation based investment that has ready access and is personally tax-sheltered from on-going investment income.

They also want flexible ownership and control and an investment structure that offers a range of investment options.

Strategy

Both Susan and John each invest separately in an Austock Imputation Bond with an initial investment amount of $125,000 each. They each contribute an additional $20,000 each year via a regular savings plan and take advantage of the 125% rule by increasing their regular savings amounts by 10% each year going forward.

Benefit

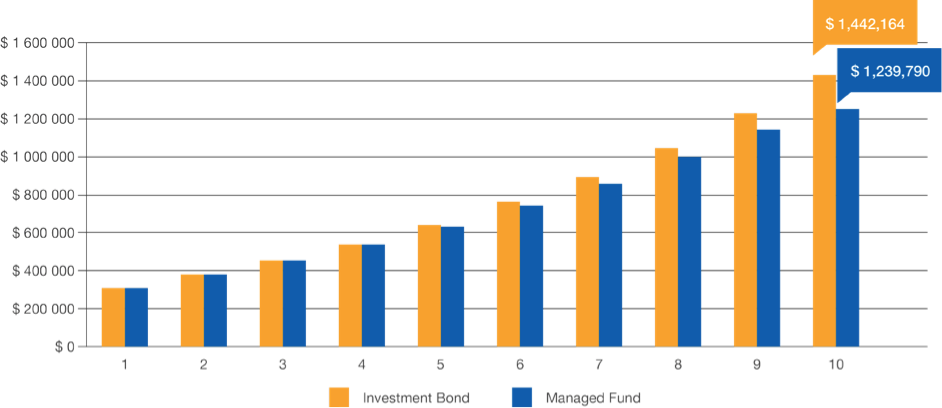

After 10 years, both Susan and John will have (combined) contributed $887,496 which they would not have been able to contribute into superannuation because their contribution limits had been reached.

Their Investment Bonds will have reached a combined value of $1,442,164 after 10 years. By contrast, if they had invested their funds into a managed fund, their combined accumulated value after tax would have been $1,239,790.

Both Susan and John are also able to access her Investment Bond benefits prior to her intended retirement age if they require.

End investment balance (after tax) after 10 years*

* Assumed annual return of 9% p.a. net of fees (5% income return, 4% capital growth) with 100% annual turnover and 50% CGT discount.

Richard Atkinson

Head of IFA Product and Relationships

Austock Life Limited

t: (03) 8601 2095

m: 0417 541 897

RAtkinson@austock.com

www.austock.com