Based on ATO data, just over 2 million Australians own an investment property. Does this mean everyone should consider if an investment property is appropriate for their wealth strategy?

Why people like property

One theory I have heard about roots of Australians obsession with property ownership stems from the First Fleet. For the first time a generation of convicts had the opportunity to be landowners as they were shipped down under. There started our cultural obsession with owning a piece of this big brown land.

Unlike any other asset class, property can be leveraged highly. For the purpose of this article, I have assumed an 80% loan-to-value ratio (LVR). The LVR measures the percentage of debt against an asset to the total value of that asset. In the below example, the purchase of a $750,000 property with a 20% cash deposit ($150,000) and a loan ($600,000) implies a LVR of 80%.

At best, shares can be leveraged by a maximum of 40% to 60% based on the lending arrangement via a margin loan or a warrant.

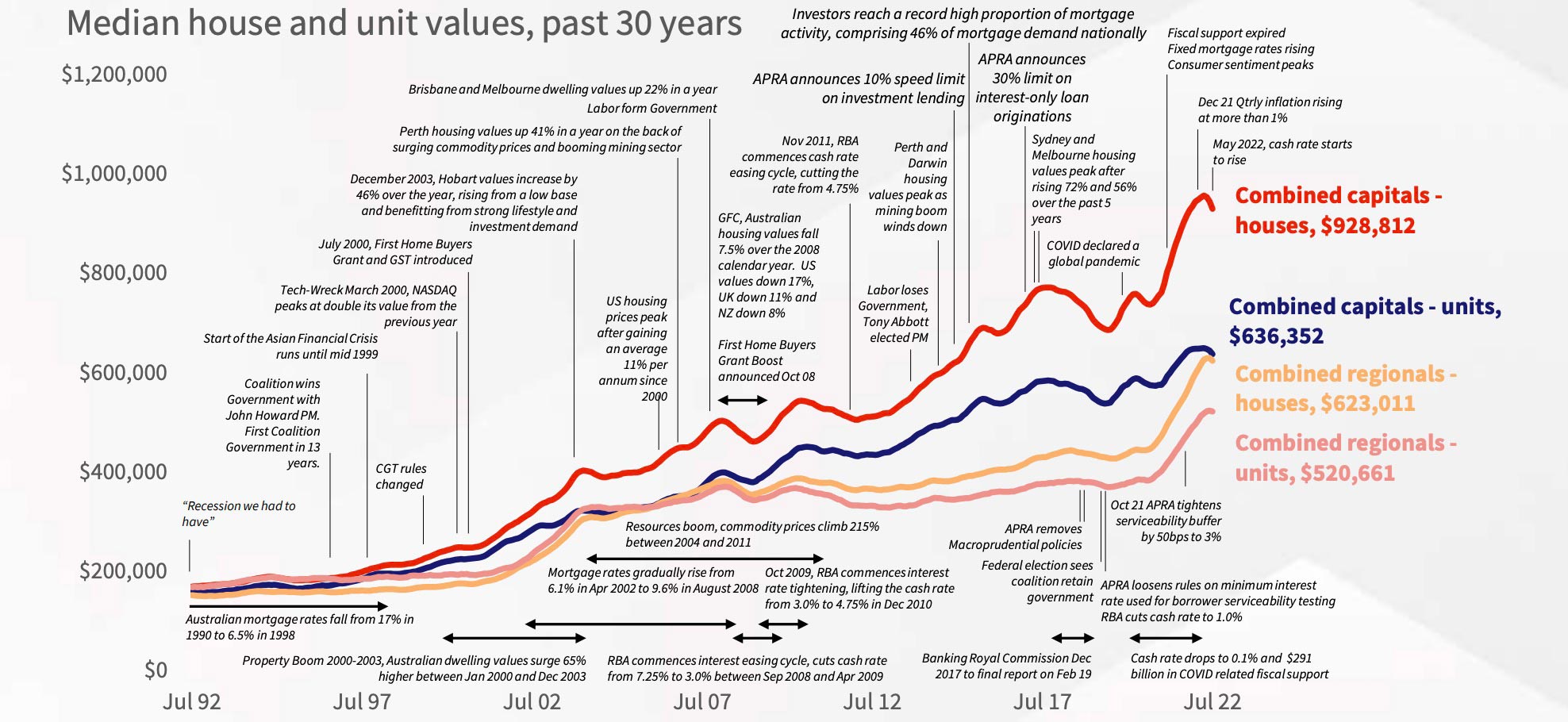

There is also a perception that property is ‘safe’ as it is bricks and mortar. However, the below chart shows that property can fluctuate in its value over time.

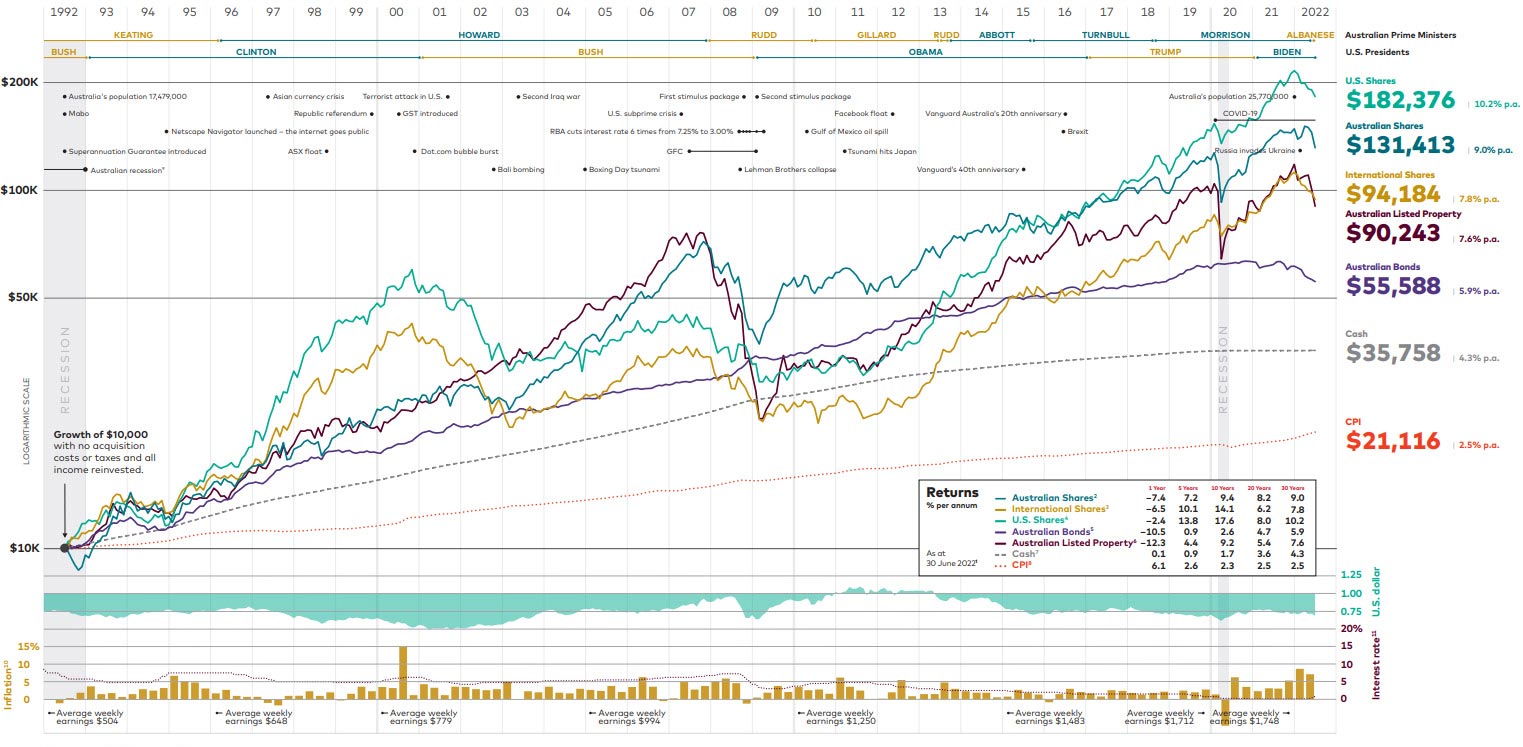

When comparing property to share markets and fixed income markets shown below, property is not as volatile, however, both asset classes trend for long-term capital growth.

When considering if an investment property is appropriate, below are some of the issues we consider:

Time frame

Based on the above chart, I generally recommend to clients that an investment in property needs a commitment of at least 10–15 years to see any meaningful capital gain. It is not abnormal for property prices to be stagnant for a 3–6 year period. If I have ever met a person who lost money investing in property, a common trend I have identified is that they held the property for under a 10 year period.

Cashflow

There are a lot of costs to consider when purchasing and maintaining an investment property. Below is a list of costs to consider:

Purchasing Costs

• Stamp Duty: Depending on which State you live this will vary. Using our $750,000 purchase scenario, stamp duty in Queensland would be around $26,775. Whereas stamp duty in Victoria would be around $40,070.

• Conveyancing costs: A Solicitor or conveyancer would assist with the purchase process. This can cost between $1,000 to $30,000.

• Incidental costs: A conveyancer or Solicitor may incur costs such as property title searches. This can be a couple of hundreds of dollars.

• Lending costs: Obtaining a loan from a bank may incur loan application fees, mortgage insurance, mortgage Solicitor’s fees, valuation fees, registration and title search fees. In my example of purchasing a $750,000 property – these fees amount to $6,860.

• Buyer’s Agent Fees: Finding a suitable investment property is not easy. If you use the services of a property buyer’s agent, these may vary between $10,000 to $20,000. Keep in mind too, if you are buying directly from a Real Estate Agent, the cost of their commission will be built into the property purchase price. It will be the vendor/seller who pays these fees to the Real Estate Agent. Property commissions can vary between 2% to 6% depending on the property.

Ongoing Costs

Owning an investment property is not simply about collecting rent and paying the mortgage. Below are some of the ongoing costs that will be experienced with an investment property:

• Agent’s fees: To have an agent manage the property in your behalf, a fee of between 6% to 9%may be payable to them. It is important to ensure that your property agent/manager is conducting regular inspections and reviewing the rent paid by the tenant each year.

• Letting fees: Each time a new tenant moves in, the property agent/manager will charge a fee for preparing the new lease. This tends to be equal to one weeks rental income for most properties.

• Council rates: As the landlord, you pay the Council Rates. This varies between $500/quarter to $1,000/quarter depending on where your investment property is located.

• Landlord insurance: What happens if your tenant damages your property? Landlord insurance will cover you for any property damage by tenants. Some of the slightly more expensive policies will cover you for ‘lost rental income’ if a tenant needs to vacate a property whilst repairs are undertaken. This can cost between $400 to $800 per year.

• Maintenance: Depending on the age of your property, any ongoing maintenance costs from changing washers in taps, fixing leaking rooks and replacing carpet is all the expense of the landlord (you). Keep in mind older properties are more likely to require more maintenance.

• Body corporate fees: If your investment property is in a strata scheme, the strata fees are your privilege of paying. This can vary between $750/quarter to $2,000/quarter in my experience.

• Land tax: Depending on how much land you own (which includes your own home), the State your property may be situation in may take your land ownership over a threshold where you are liable to pay land tax. This can be a couple of thousands of dollars each year. Your Accountant will be able to confirm prior to purchase if you will be exceeding any land tax thresholds and therefore liable to pay land tax.

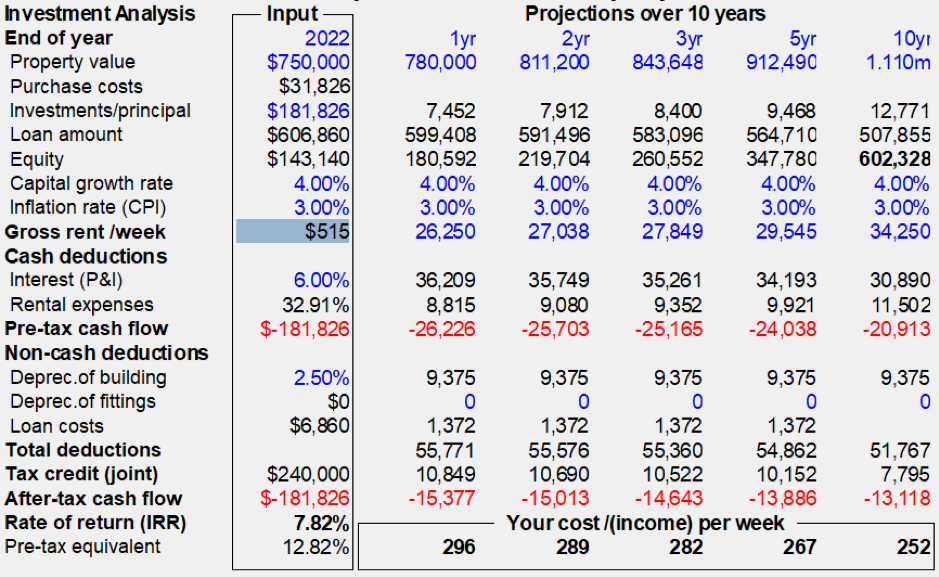

Below is a summary of the cash flow for an investment property

Based on a $750,000 purchase price, this property is rented at $515/week. After all expenses the weekly holding cost (the negative cashflow you must cover) is approximately $296 per week.

Negative gearing

Many people I have met cite the ‘benefits’ of negative gearing as a reason why they purchased an investment property. Let’s get this right: if you purchase an asset that loses you money as the income does not cover the expenses, you can claim a tax deduction against other income that you earn. Your investment property is still ‘losing’ you money to own. Therefore, with such a strategy you are relying on capital growth to make the overall strategy worthwhile. In our example above, the loan would need to be reduced from $600,000 to $310,000 before the property become cash flow neutral.

It is important that if you are purchasing an investment property, that you are comfortable that you can service the holding costs of such an asset.

Future Capital Gains

Choosing the correct ‘entity’ to own an investment property is crucial. This will impact what your tax liability may be when you sell your property in the future. For example:

- Personal ownership: Capital Gains Tax will always be your marginal tax rate which can be as high at 47% including Medicare Levy.

- Company ownership: Tax will be 30% and you do not benefit from the 50% Capital Gains Tax discount if you held the property for more than 12 months.

- Trust ownership: Ultimately, the tax rate applied to any capital gains will be the marginal tax rate of the beneficiaries of the Trust. Again, this can be as high as 47%.

- Self-Managed Superannuation Fund (Accumulation phase): If you own a property in your Self-Managed Superannuation Fund and you are still working, tax on capital gains is 15% if the property was owned for less than 12 months or 10% if the property is owned for more than 12 months.

- Self-Managed Superannuation Fund (Pension phase): If you are retired and drawing an account based pension from your Self-Managed Superannuation Fund, any capital gain on the sale of an investment property is TAX-FREE!

Strategy

In summary, here are my quick tips to see if an investment property is appropriate for your wealth creation strategy:

- Hold the property for the long-term (10-15 years).

- Ask yourself, can you afford repayments at higher interest rates?

- Keep a cash buffer of at least 6 months of rental expenses and loan repayments in the event that your tenant vacates or you lose your job.

- Consider your ownership entity before purchasing. It is expensive to change ownership structures once you have purchased an investment property.

- Sell when your personal income is low (Typically once you are retired)

- Get advice from a Mortgage Broker, Accountant and Financial Adviser to ensure such a purchase is appropriate for your wealth creation strategy.

Assumptions:

- Property purchase price: $750,000

- Cash deposit paid $150,000

- Stamp duty (NSW) and purchase costs paid with cash $31,826

- Loan: 6% interest rates. 30 years period. Principle and interest repayments.

- Capital growth assumption 4% per annum

- Rental yield 3.5% per annum or $515/week

- Rental expenses pa:

- Agents’ fees 8%

- Letting fees $515

- Council rates $2,500

- Landlord insurance $450

- Maintenance $250

- Body corporate fees $3,000

- Building depreciation claimed at 2.5% pa

- Assumed 50:50 ownership between two people earning $150,000 and $90,000 pa respectively.

Andrew Zbik

Senior Financial Adviser

Creation Wealth

0422 038 253

andrew.zbik@creationwealth.com.au

www.creationwealth.com.au