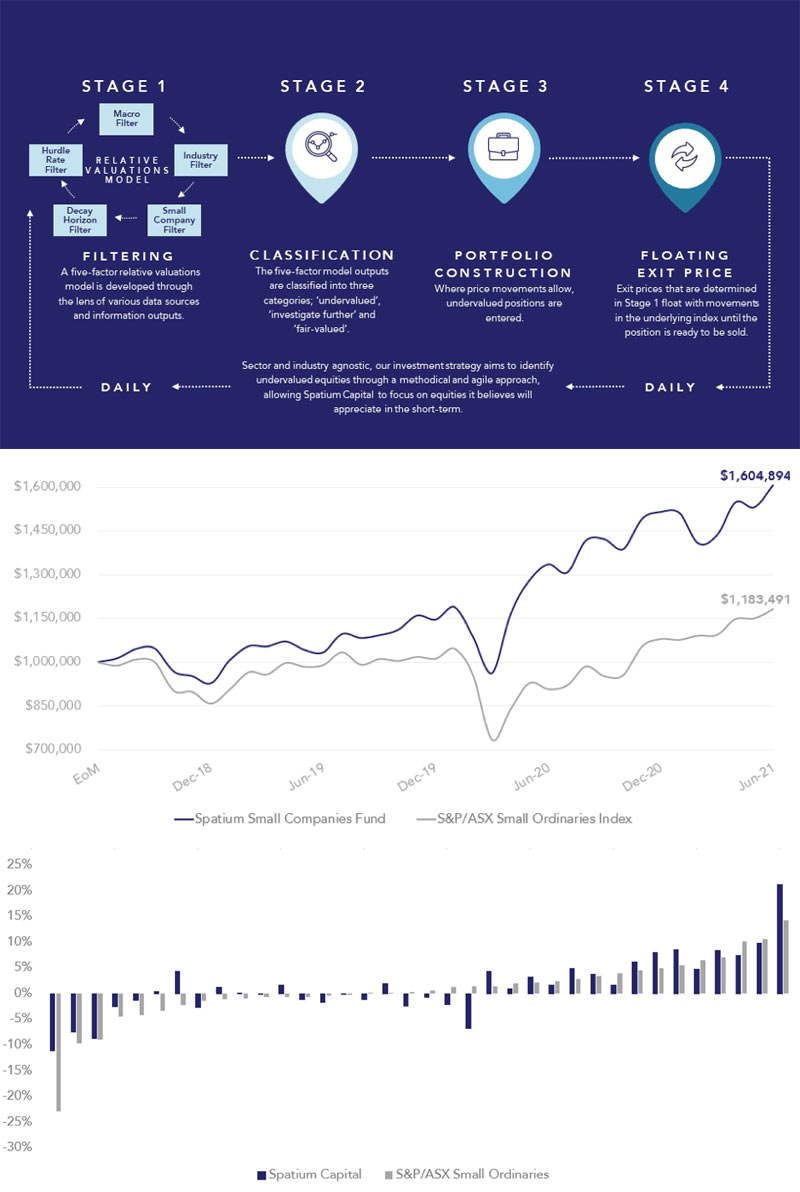

Since inception on 1 July 2018, Spatium Capital has returned 17.1% per annum (after fees) over a three-year period versus the S&P/ASX Small Ordinaries benchmark (‘benchmark’) return of 5.8% over the same horizon. This equates to an annualised outperformance of 11.3%.

A key focus of Spatium’s approach is the ability to preserve investors’ capital, which was exhibited throughout the course of 2020. As financial markets were beset by volatility following the COVID-19 outbreak, the fund manager preserved investors’ capital whilst exceeding the benchmark, returning 32.2% for the calendar year where the benchmark closed up 6.6%.

In a segment of the market that has historically had a marginally higher risk profile than the blue-chip stocks, Spatium seeks to be a consistent outperformer of the small cap landscape with a lower risk profile than the benchmark.

In a segment of the market that has historically had a marginally higher risk profile than the blue-chip stocks, Spatium seeks to be a consistent outperformer of the small cap landscape with a lower risk profile than the benchmark.

By managing a broad, diversified portfolio of companies (an average of 25 to 40), and actively rotating its portfolio, on average, every 30 to 45 days, Spatium is strategically placed to capture potential upside in the small cap segment of the ASX.

Target exit prices inform Spatium’s ‘shopping list’

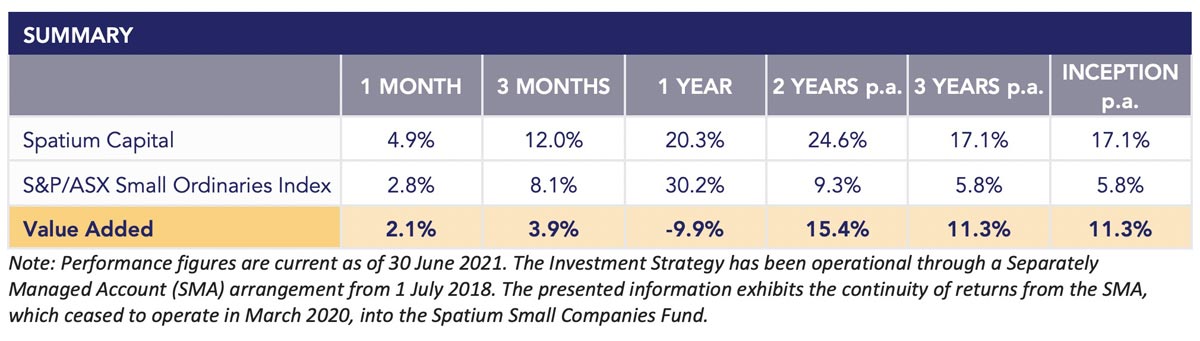

Spatium’s long-only approach begins with forming a view of each company on the ASX 300 relative to the benchmark. In this assessment, a five-factor relative valuations model is constructed (see graphic below) which applies a series of hurdles to remove companies viewed as fairly valued and unlikely to offer short-term upside value to the portfolio.

Companies satisfying each of these hurdles are then investigated further (approximately 60 to 80 listed companies are cycled through this range) and target entry prices are developed for each. At the same time, target exit prices are prepared for each position. With these price targets ready, a ‘shopping list’ is prepared of companies to be executed during the course of the market day.

Not every company Spatium seeks to hold will fall below its target entry price, and a position will therefore not be taken in these companies. When this occurs, focus moves to the next opportunity that both trades below the target entry price and offers potential upside to the portfolio. Finally, each position is held on an equally weighted basis, which Spatium believes removes any bias for ‘falling in love’ with a particular company, its management team or its product.

Whilst past performance is not indicative of future performance, in a market that is becoming increasingly filled with speculation and prone to emotional responses, Spatium believes its approach to managing the portfolio in this way, enables agile and timely reactions to opportunities as and when they occur.

Note: The above bar chart highlights Spatium Capital’s returns across the S&P/ASX Small Ordinaries worst and best months (left to right) over the last 36 months. In both the extreme left and right cases, Spatium Capital has demonstrated an ability to preserve capital (the extreme left) whilst also outperforming strong markets (the extreme right).

This approach to generating returns is however not without its limitations. Spatium’s ability to find opportunities and hold an equally-weighted portfolio of companies, mostly within the ASX 101-300, is contingent on staying dynamic and agile. In protecting this ability to remain agile, the Spatium Small Companies Fund will not seek to grow total funds under management greater than $160 million.

Benefits to SMSF investors

The ability to identify a mispriced – that is, undervalued – company is requisite to capitalising on their potential upward movement back to fair value.

In the years since securing its first cornerstone SMSF investor, Spatium has seen many SMSFs, high-net worth investors, endowments and private businesses diversify their investments by allocating a portion of their funds to the Spatium Small Companies Fund.

Jesse Moors

Director | Operations

Spatium Capital

0422 040 119

jesse.moors@spatiumcapital.com

Nicholas Quinn

Director | Investments

Spatium Capital

0437 175 038

nicholas.quinn@spatiumcapital.com