The growth in use of reverse mortgages by asset rich, cash poor seniors is increasing rapidly. As is the awareness by their children that this new debt facility will decrease their inheritance. Seniors receiving their lump sum will mean that the house that now has a reverse mortgage against it is having a capitalised charge against its future value. The children’s inheritance (i.e. the family home) is losing equity by the cost of the interest being charged by the lender.

The growth in use of reverse mortgages by asset rich, cash poor seniors is increasing rapidly. As is the awareness by their children that this new debt facility will decrease their inheritance. Seniors receiving their lump sum will mean that the house that now has a reverse mortgage against it is having a capitalised charge against its future value. The children’s inheritance (i.e. the family home) is losing equity by the cost of the interest being charged by the lender.

ASIC figures suggest that a $1,500,000 house with a $300,000 reverse mortgage loan will increase to more than double over 15 years.

What can the children do to make an ‘investment’ in protecting the tax-free inheritance that is available via their parent’s home?

Case study: Ian and Rosie take out a reverse mortgage and the kids pay the interest to protect the value of the home

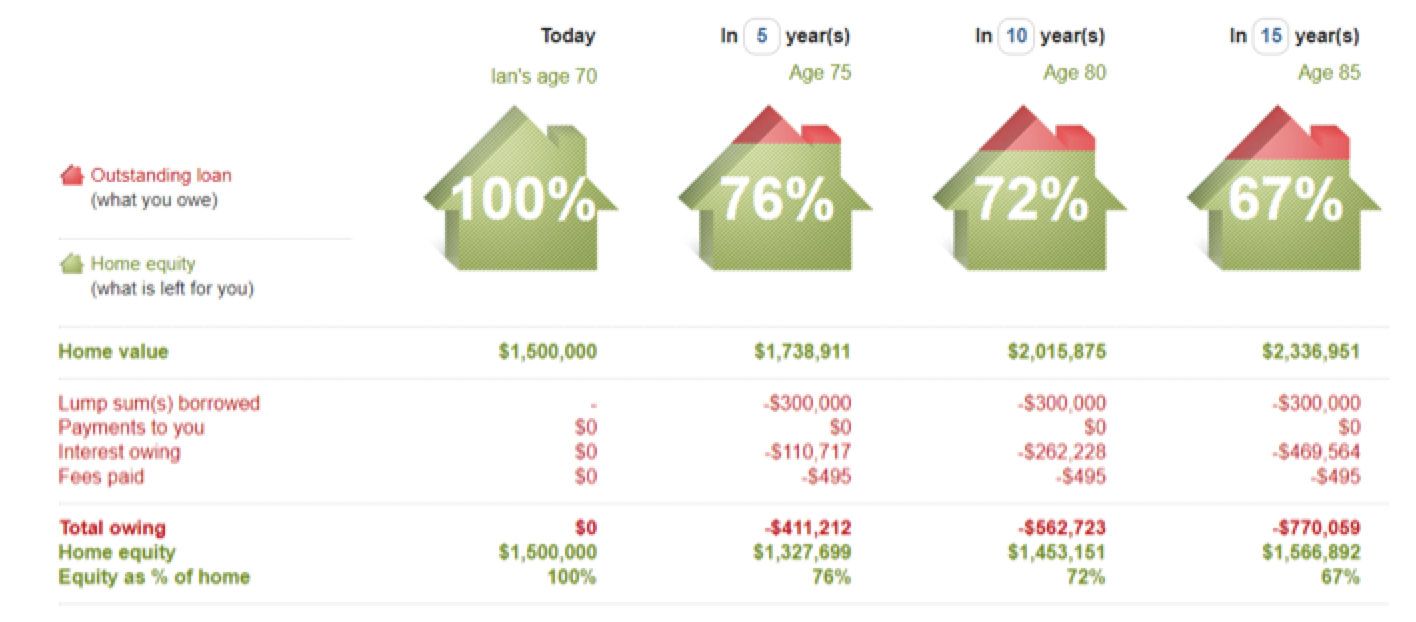

Ian and Rosie have an unencumbered property in Sydney valued at $1.5m. Both are 70 years of age and on the Age Pension.

They needed $300,000 to complete renovations, have a regular pension top-up and they also wanted to take their grandchildren on a holiday.

Ian and Rosie discussed with their two children that they are considering taking a reverse mortgage loan. At age 70 they would be eligible for 25% of the value of the home as a loan with a 6.29% interest rate. (Properties below $2mil incur $495.00 fees and charges, this includes valuation and settlement fees.)

Normally, there are no repayments required with reverse mortgage loans.

However, their children decided that they would contribute the interest only component or any contribution equally between them, so the loan amount does not increase and the impact on their inheritance is minimum. Going by the property trend the growth is approximately 3% per year. See chart below.

ASIC Reverse Mortgage Moneysmart Calculator

This section estimates remaining equity with different assumptions about future house value and interest rates.

This is an estimate, not a guarantee. You may end up with more or less equity in your home.

- Carefully discuss and consider with a financial planner, lawyer and Centrelink of any financial impact on your pension or superannuation.

- Seek independent financial advice

- Make sure all costs associated with the loan are assessed

- Ensure there is no obligation to purchase any other product or service to receive an equity release product (Reverse Mortgage)

- Seek advice to update your Will

What is a reverse mortgage?

It will allow you to borrow against the equity in your home without having to sell, by releasing funds for comfortable years ahead in retirement.

It is a loan available to homeowners, 60 years or older, which allows them to convert part of the equity in their home into cash.

It can be taken against the family home as well as investment properties.

Safeguard you and your property by choosing the right reverse mortgage

- Ownership of your home stays with you

- Protect the amount of equity left in your home at the end of the reverse mortgage (most people have chosen up to 50% of home equity protection which becomes available to the Estate)

- Repayments are not required, however, you can make payments big or small at any time and be able to redraw

- Ensure you receive independent legal advice

- Ensure you receive independent financial advice

- Involve the family and other beneficiaries in the decision.

Ambreen Sumar

Reverse Mortgage and Aged Care Lending Specialist

Omniwealth

m: 0400 243 259

ambreen.sumar@omniwealth.com.au

www.omniwealth.com.au