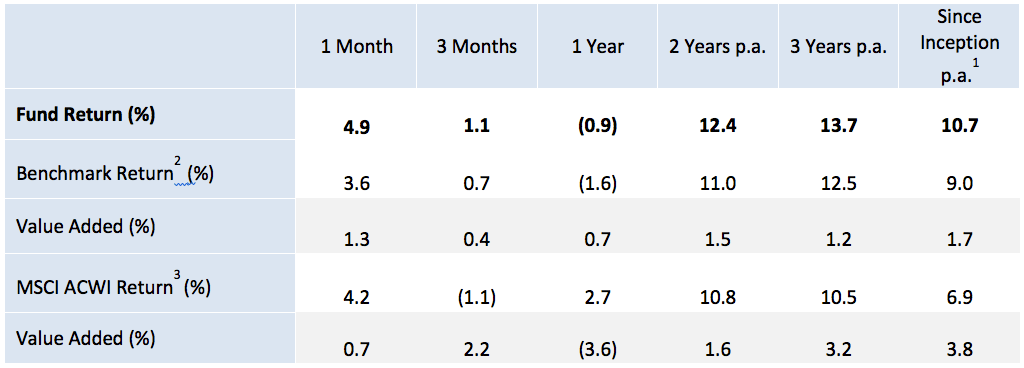

The Nanuk New World Fund returned 4.9% in January, outperforming traditional global equity benchmarks such as the MSCI ACWI which rose by 4.2% (all returns quoted in AUD unless specifically stated otherwise).

Performance Summary1 (AUD)

Industry commentary

The acceleration of the global energy transition continues as we enter 2019, uninterrupted by concerns of slowing global economic growth and market volatility evident at the end of last year. Policy commitments are being strengthened, positive industry developments continue and legacy technologies struggle in the face of rapid change.

In Europe, France announced €30b of subsidies for clean power over the next decade and Italy’s Ministry of Economic Development outlined plans for the development of 50GW of solar and 20GW of wind by 2030. India’s Ministry of New and Renewable Energy, meanwhile, announced a hugely ambitious target of 500GW of renewable generating capacity by 2030 (representing around 60% of total national generating capacity at that point), of which solar and wind will account for 350GW and 140GW respectively. The plans are an extension of the existing 2022 target of 100GW of solar and 60GW of wind. Achieving these ambitious targets will require tendering for 30GW of solar and 10GW of wind capacity annually. (For comparative purposes 1GW is typical of the capacity of a large coal or nuclear fired power station).

Germany’s Coal Commission submitted its recommendations for phasing out coal power which would see coal-fired electricity generation decline to zero by 2038. The plan was broadly in line with investor expectations and cautiously welcomed by utility executives. In the US, the Energy Information Administration reported an acceleration in coal plant retirement, with almost 14GW forecast to close during 2018, second only to 2015’s record. This comes despite the Trump administration cancelling President Obama’s Clean Power Plan.

Continued progress in the wind industry was highlighted by Vestas’ (the global leader in onshore wind turbines, a Fund investment) unveiling the largest and most powerful onshore turbine ever. Its new 5MW platform is built around a modular architecture to improve costs efficiency and will produce 26% more energy than current benchmark turbines. Siemens Gamesa (the leader in the offshore wind turbine market, also a Fund investment) released details of its own record-breaking machine, a giant 10MW offshore wind turbine with a rotor diameter of 193 metres. Andreas Nauen, CEO of its offshore wind division said the offshore wind sector was at a tipping point, reflected in company expectations to build 400 offshore turbines in 2019 – more than it has delivered during the previous 8 years combined.

China’s National Energy Administration reported further significant declines in curtailment of renewable energy. Curtailment occurs when generation exceeds the capacity of the grid to dispatch that power, either through lack of demand or lack of transmission capacity. Chinese wind and solar generators have suffered high curtailment rates in recent years because much of their renewable generation is in remote provinces such as Inner Mongolia and Xinjiang, where power consumption is low and transmission to meet demand in other parts of the country has been constrained by lack of infrastructure. China has addressed this with massive investment in transmission infrastructure to export the power towards population centres, as well as policy support to promote prioritisation in the use of renewable generation. The latest data indicates this is working. Curtailment for wind fell from 7.2% in 2018 to 4.9% in 2019, and for solar from 6% to 3% respectively.

Meanwhile the challenges faced by traditional energy businesses continue. California’s largest utility, Pacific Gas & Electric, filed for bankruptcy protection, following lawsuits charging it with causing some of the fires that raged through the state last year. The PG&E Corporation had over $70b in assets at its last reporting date, so this was a staggering outcome. Elsewhere the nuclear sector’s challenges continued as Hitachi suspended development of two nuclear reactors in the UK, booking a loss of $2.7b in the process. In more positive news, Bloomberg New Energy Finance reported corporate offtake for renewable energy had more than doubled in 2018, to 13.4GW. Facebook was the biggest off-taker, with 2.6GW.

As a testament to rising awareness of sustainability in the fossil fuel industry, oil giant Baker Hughes announced a commitment to halve its carbon emissions by 2030 and eliminate them altogether by 2050. Notably, CEO Lorenzo Simonelli said that move came because “customers want us to move in that direction”. Oil producers continue to invest in technologies for a post fossil fuel era too, with BP announcing an investment in Chinese EV charging business PowerShare, and Shell announcing an investment in AutoGrid, a start-up developing ‘grid flexibility’ software to manage the integration of renewable generation.

In the automotive sector, Panasonic, which supplies Tesla with batteries, announced a battery joint venture partnership with Toyota. Ford announced that it is working on an electric version of its iconic F-150, America’s multi-decade best-selling vehicle. Also in the US, Colorado is set to become in the 10th state to follow California in adopting a zero emission vehicle (ZEV) mandate. California’s ZEV target of 9% of new vehicle sales by 2025 has become the benchmark for other states looking to act in the absence of policy leadership from the Trump Administration. Meanwhile, Amazon commenced a trial of autonomous package delivery vehicles in suburban Seattle using sidewalk-bound, six-wheeled electric robots.

Market commentary

Global equities recovered sharply in January from December’s fall with the MSCI All Country World Total Return Index rising 7.9% in US dollar terms. The VIX index, a measure of expected volatility in the US market, declined by a third over during the month; Brent crude oil appreciated by 15%; and the JP Morgan Emerging Market Currency Index rose 3%. Regionally, all major equity indices rose. The US’ S&P 500 Index was up 7.9%, Hong Kong’s Hang Seng Index was up by 8.1%, Europe’s Stoxx 50 Index gained 5.3% and Japan’s Nikkei 225 Index was up 3.8%. Environmental Equities underperformed slightly, with the Fund’s benchmark, the FTSE Environmental Opportunities All Share Total Return Index, up 7.3% in US dollar terms trailing the MSCI ACWI by 0.6%. In Australian Dollar terms the Fund returned 4.9% in January, outperforming the benchmark FTSE Environmental Opportunities All Share Total Return Index which posted a 3.6% return for the month.

Macroeconomic news was mixed. The Federal Reserve signalled that it would pause monetary policy tightening, responding to weaker US economic data late in 2018. Notwithstanding this, and the longest government shut-down in US history continuing for most of January, the US labour showed continued growth in both employment and labor force participation, modest real wage gains, and steady productivity growth. Elsewhere, China reported disappointing Manufacturing PMI data, with back-to-back readings below 50, indicating contraction. PMIs in Japan and Europe also fell, albeit remaining just above of 50.

Fund commentary

The Fund returned 4.9% in January, outperforming its benchmark index by 1.3%. The largest contributions came from the Fund’s position in wind turbine manufacturers Siemens Gamesa Renewable Energy and Vestas Wind Systems, automotive component suppliers including Lear Corporation, and in companies exposed to the semiconductor industry, including collaborative robotics leader Teradyne. The contribution from positions in cyclical sectors reflected the strong recovery in many stocks that had underperformed in the second half of 2018. Several recently-added or increased Fund investments including specialist waste management business Stericycle, energy efficient water heater manufacturer A.O.Smith and US building materials company Owens Corning contributed positively to January performance.

Despite slowing global economic growth and geopolitical issues – and in particular the US-China trade dispute – continuing to present risks, many areas within the Fund’s investment focus are likely to see strong growth in 2019. Annual global solar and wind installations are forecast to rise as much as 17% and 27% respectively. Battery energy storage systems are likely to see 50-100% growth in response to falling prices and subsidy programs. Passenger electric vehicle sales are forecast to grow around 40% in 2019 – new model releases driving EV’s towards 3% of the total global market. The demand for collaborative robots is expected to grow by around 40% this year – despite the global slowdown in industrial automation investment.

With equity market valuations at the start of 2019 at more normal levels, the Fund has made a number of new investments in companies with exposure to areas of medium to longer term secular growth that significantly underperformed during 2018 that now offer potentially attractive returns.

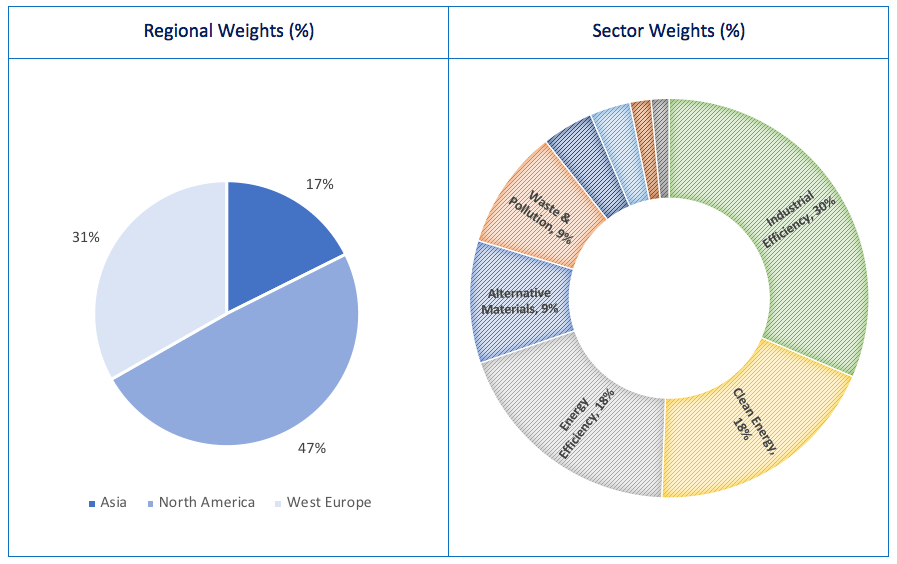

At the end of January 2019 the Fund’s largest sector exposures are in the industrial internet of things, building energy efficiency, high speed rail, advanced and sustainable materials, industrial automation, waste management, automotive efficiency and the wind energy sector.

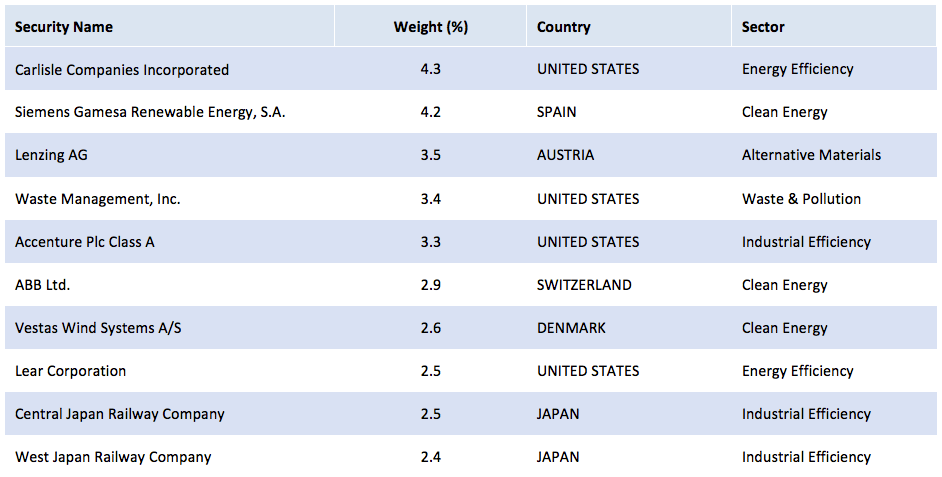

Top 10 Holdings as at 31 Jan 2019

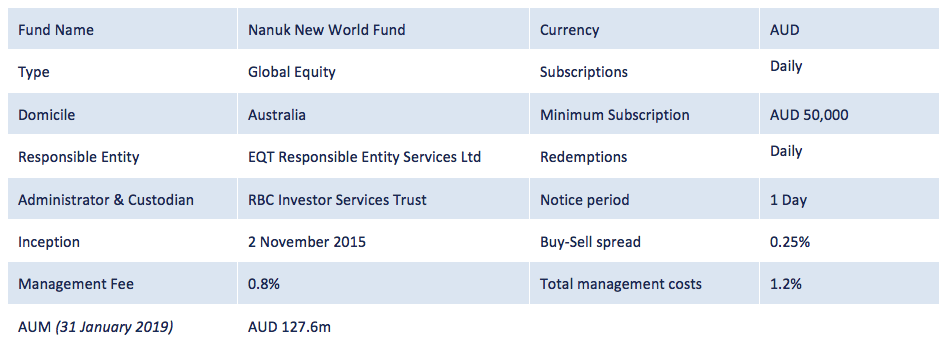

Fund Details

Dan Powell

m: 0419 914 212

e: enquiries@nanukasset.com

www.nanukasset.com