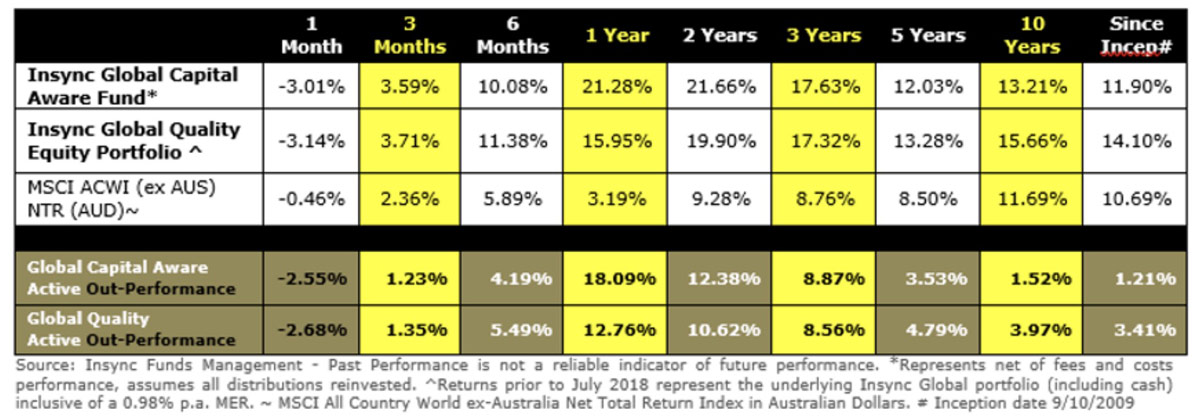

Insync October Fund Commentary

The last few weeks of the month witnessed stronger performance from the Value and more economically-sensitive sectors, versus the companies we typically invest in. This is the usual market ‘exuberant reaction’ driven mainly by the latest hopes of a vaccine, optimism of a huge fiscal stimulus in the US following a Democratic win and what was then a possible Democratic easy sweep. A sawtooth pattern emerges in cyclicals at times such as this where they surge above the market for a short period. Thus, we underperformed in the month but easily maintained excess performance across all other time periods.

Insync’s strategy of investing in 30 super-profitable businesses, across 16 global megatrends with little sensitivity to global GDP, continues to deliver consistent outperformance.

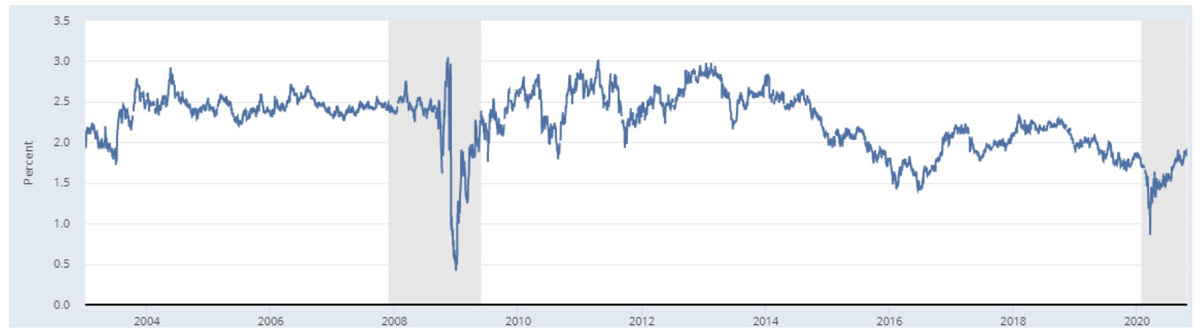

A notable feature of the current investment cycle from the lows of the GFC has been the severe underperformance of the ‘Value’ factor. The world economy just cannot escape its low-growth, low-inflation rut. This remains as a significant headwind for Value-driven stocks. The emergence of Millennials and Gen-Zers is playing a greater role in shaping the future but is also counterbalanced by an ageing population. This tends to produce a deflationary impact. There is a strong relationship between a rising old-age dependency ratio and low inflation.

Whilst there is growing optimism on a reflation trade, the 5-year inflation expectations continue to remain low.

This is not surprising as aggressive central bank policies to drive up growth and inflation over the past 10 years have largely failed. Whilst a more aggressive fiscal policy may well increase growth in goods and services inflation in the short term, the secular deflationary drivers of an ageing population and technology are likely to remain dominant.