Objectives-Based Investing (OBI) or Goals-Based Investing describes not only an investment philosophy, but also a method of implementation that sets it apart from traditional financial planning.

When I read about OBI, I can hear financial planners saying to themselves “yes, that’s what I do because that’s what financial planning is (and always has been) about.”

So why are people making such a big fuss over words and phraseology?

Most financial planners approach the advice process with the goal of understanding their client’s objectives and then formulate a plan to work toward the realisation of the stated goals and objectives over time. I did (and continue) to do so today, however, with one very important distinction … my clients now also understand, and can articulate why we are doing what we are doing.

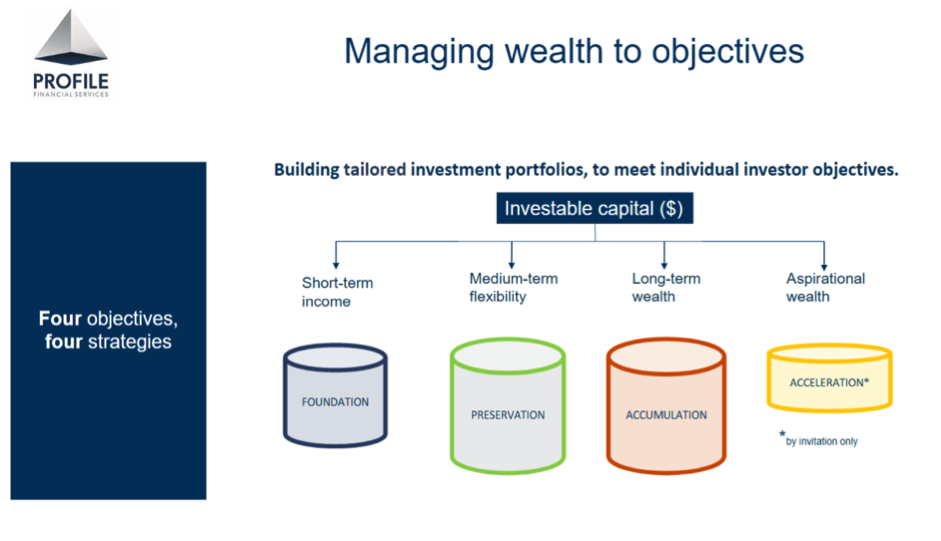

One of the important tenets of OBI is that investment objectives need to be allocated specific timeframes. In doing so, clients begin to understand their portfolio as groups of funds set aside to meet specific objectives in specific timeframes. A sure-fire way to destroy wealth is to be forced to sell an asset at an inconvenient time, at a compromised price. The OBI approach ensures clients’ short-term income needs are covered using conservative assets such as cash, so that in times of market stress they are not forced to realise paper losses in order to pay the bills.

The three key risks that our clients identified they wanted addressed in their plan were:

- Ensure I have sufficient cashflow to meet my required day-to-day living expenses

- Ensure that I can meet unforeseen expenses as and when they may arise, without the need to have to sell longer term growth assets.

- Ensure that I do not run out of money in my lifetime.

Profile set about building a tool (which we call Profile Pathways) that allows advisers to clearly demonstrate to a client how their stated objectives can be met by allocating their investment capital across agreed timeframes in a systemic manner. Further, it allows an adviser to demonstrate the level of risk that the client needs to undertake to meet their objectives.

“I believe that advisers are well credentialed to articulate why a client might need to increase their allocation to growth assets, to meet their objectives. However, I do not feel advisers are as adept at demonstrating situations where a client can take on less risk and still meet their objectives.” This is best demonstrated in the following client case study.

“Kathy (and her late husband Charles) have been clients since 2005. They were asset rich and income poor when we first met, and with retirement pending, they were seeking advice on how to restructure their financial situation to ensure that their retirement income objectives could be met.

“We provided them with a plan and duly implemented it over the years. In 2011, we formally adopted the OBI philosophy and introduced it to Kathy for her consideration. We explained the OBI philosophy by way of a “bucket diagram” (see below) which allowed Kathy to understand and appreciate why specific amounts were being allocated to each timeframe ‘bucket’,” said Phillip Win, Managing Director, Profile Financial Services.

Each of the buckets has a target rate of return that is used in the modelling. The underlying assets are selected for each of the buckets based on meeting that rate of return within a given timeframe. The underlying assets’ projected volatility is also considered. Because the Accumulation bucket has a higher target return and a longer timeframe than say, the Preservation bucket, it tends to hold more growth-oriented assets.

Kathy advised us of her required income in retirement and her anticipated capital expenditure over the foreseeable future. These inputs were then used to calculate the allocation to each bucket.

The following table illustrates the standard, recommended and current allocations to each of the buckets.

| Standard | Recommended | Current | |

|---|---|---|---|

| Foundation | 18% | 18% | 20% |

| Preservation | 29% | 64% | 80% |

| Accumulation | 53% | 18% | 0% |

Each of the above outcomes resulted in Kathy meeting her stated objectives, however, you see that the ‘standard’ allocation would have resulted in her taking on more risk. Yet, her investment capital would have grown more, however, this was not a stated objective and hence the recommendation to re-allocate the buckets to minimise risk and still meet the agreed objectives. The table suggests a decrease of 35% to the Accumulation bucket. The beauty of having Profile Pathways to illustrate the basis (or why) this was possible was invaluable.

“Each year, we re-run the model to ensure that the allocations remain appropriate and that any new objectives, and changes in markets, are accounted for in the model. This has resulted in there no longer being a need for Kathy to have any exposure to higher-risk Accumulation type assets to achieve her goals.

“Kathy feels comfortable knowing that excessive risk is not being undertaken to meet her objectives and she has no fear of running out of money in her lifetime,” said Mr Win.

Phillip Win

Managing Director, Senior Financial Planner

Profile Financial Services

T: 02 9683 6422

M: 0408 728 849

phillip.win@profileservices.com.au

www.profileservices.com.au