Investment Bonds have benefits and features which are worthwhile evaluating as a way to supplement superannuation or even as an alternative tax-effective vehicle.

Tax effective structure of Investment Bonds

Investment Bonds are tax-paid investments similar to superannuation. Throughout a Bond’s investment term the Investment Bond pays tax annually on behalf of the investor at a maximum tax rate of 30%.

This can provide valuable tax rate “arbitrage” benefits due to the difference between an investor’s higher ongoing personal marginal tax rate and the Investment Bond’s effective (lower) tax rate.

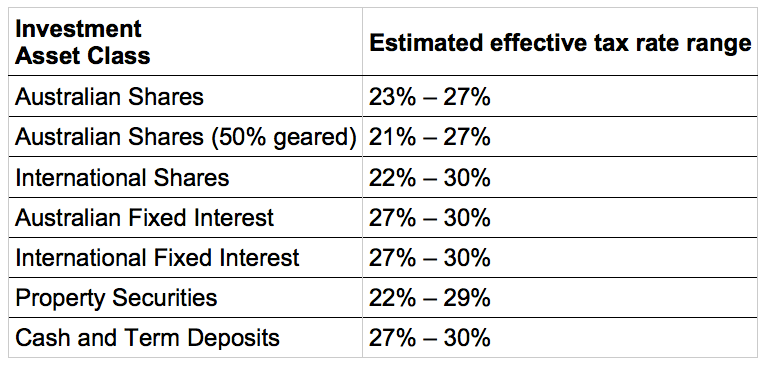

In the case of Austock Life’s investment portfolio options, each has its own tax rate which is nominally stated as 30%. From year to year and depending on the asset class invested in, the level of imputation and foreign tax credits and tax provisions, the actual effective tax rate can be significantly less.

The table below shows estimated, long-term tax rate ranges for Austock Life’s different investment portfolio asset classes.

Accessibility

Investment Bonds provide unrestricted access to benefits with no preservation age, retirement or purpose test required.

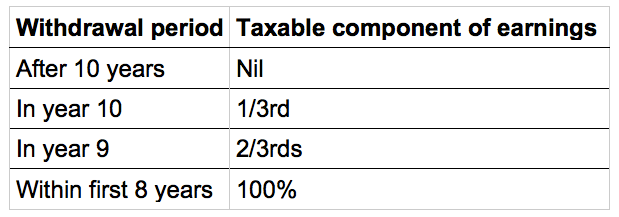

Proceeds received from partial or full withdrawals made after 10 years are considered a tax-free receipt and not subject to personal income tax or capital gains tax. Where an investor fully or partially withdraws from an Investment Bond within the first 10 years of investment, the earnings component will generally attract personal tax.

The apportioned earnings included in the withdrawal will be assessable as follows.

A 30% tax offset entitlement is available to reduce the amount of tax (if any) payable by the investor.

Investment Bonds also have the added flexibility of being able to be transferred to another person or entity with the original investment date carrying over for the purpose of the 10-year period.

No limits or caps on the investment amount, unlike superannuation

Unlike superannuation, there are no work-test or aged based restrictions on investing, so that those over age 65 years can continue to make investment contributions. Restrictions such as non-concessional contribution caps and concessional contribution caps that limit or penalise excess contributions do not apply.

There are no caps on the amount that can be invested in an Investment Bond. You can progressively increase an Investment Bond’s tax-effectiveness by making ongoing contributions under the taxation law applicable to Investment Bonds, known as the 125% Rule.

Under the 125% Rule, the Investment Bond’s valuable taxation status is maintained when making ongoing additional contributions, provided these do not exceed 125% of the level of contributions made in the immediately preceding 12 month period.

The attraction of the 125% add-on feature is that you can make ever increasing levels of additional contributions. This can be done at any time during and even beyond the Investment Bond’s initial 10-year period.

Investment options

You can construct the Investment Bond’s investment mix by using one or multiple investment portfolios from a range of passively (index) and actively managed funds covering all asset classes including cash, shares, fixed interest, and property.

The Investment Bond’s switching facility provides the flexibility and tax-freedom to change the investment portfolio mix at any time to suit changing circumstances or market conditions, without personal tax or capital gains tax consequences.

Estate planning

Under superannuation legislation, death benefits must be made payable to a “dependant” as provided for under the legislation. Beneficiaries that an investor nominates must be proven to be a dependant of the investor, otherwise death benefits may not be paid to the person, and instead paid to the estate and be subject to tax.

Beneficiaries nominated under an Investment Bond are not required to be a dependant. As such, there is no restriction on who can be nominated as a beneficiary, which may include a person, company, charity or trust.

There is also no requirement to nominate or re-nominate a beneficiary every three years in order to make the nomination binding (unlike many superannuation funds). The death benefit from an Investment Bond is paid tax-free to the beneficiary, irrespective of who the beneficiary is…no death benefit tax is payable.

Tax reporting

Similar to superannuation, using an Investment Bond removes the ongoing accounting, tax management, regulatory and legal costs for an investor. Investment Bond investors are not required to report on or pay PAYG instalment tax for the term of their investment.

In addition, investors are not required to maintain tax records or make annual tax declarations (unless a withdrawal is made within the 10 year period).

There is also no requirement to provide a tax file number or maintain detailed cost base, capital gains tax and imputation credit records that are typically required with other investment structures. In addition, no withholding tax is required to be paid on earnings (including for foreign resident investors).

Richard Atkinson

Head of IFA Product and Relationships

Austock Life Limited

t: (03) 8601 2095

m: 0417 541 897

RAtkinson@austock.com

www.austock.com