Do you have a self-managed superannuation fund (SMSF) with a balance under $500,000, are not yet retired but some unexpected life events have halted your ability to contribute more to your SMSF?

This may have been the result of a redundancy, career change that has not gone to plan, or change to a lower level of income.

Research by ASIC shows that SMSFs with assets under $500,000 may have lower returns after expenses and taxes compared to industry or retail Superannuation Funds.[1]

SMSFs can provide additional strategies not available in an industry or retail fund. These include:

- Being able to borrow money and purchase residential investment property.

- Being able to borrow money and purchase a commercial or industrial property and lease to a business you own or operate.

- Being able to lend your own money to your SMSF to purchase property or shares.

- Control over where your Superannuation is invested in non-traditional asset classes such as currency, cryptocurrency, collectables, and unlisted companies.

- More flexibility with controlling estate planning outcomes.

If your SMSF strategy is not using one of the above options and is simply invested in a diversified portfolio similar to what can be offered in an industry or retail superannuation fund, there may be a point in time to reconsider if an SMSF is still the appropriate structure to manage your superannuation if your assets are under $500,000 and it looks like you won’t be able to contribute further to your SMSF for a number of years.

The cost of maintaining a SMSF in my experience is generally as follows:

- Between $1,500 to $2,000 per annum for accounting fees to complete an SMSF tax return and financial statements

- Between $250 to $500 for an SMSF audit

- ATO supervisory levy of $259

- ASIC annual filing fee of $273.

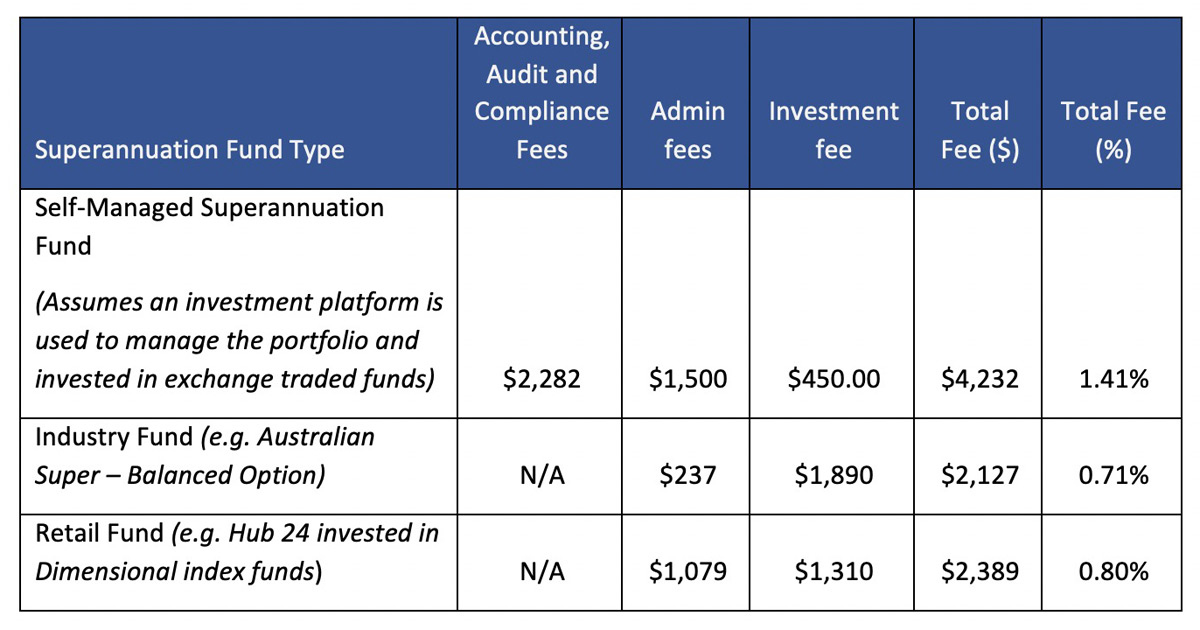

Thus, the cost of compliance for an SMSF varies between $2,282 and $3,032. In some instances, this can be even higher.

If you have a small, diversified investment portfolio in your SMSF, for example $300,000, some alternative options may be:

Fees are not the only factor to consider when determining which superannuation fund structure may be appropriate for your needs. However, if you are using an investment strategy that is very similar to what can be offered in an industry or retail superannuation fund, there may be a point in time to accept that you are not using the ‘additional’ features an SMSF can provide.

Fees are not the only factor to consider when determining which superannuation fund structure may be appropriate for your needs. However, if you are using an investment strategy that is very similar to what can be offered in an industry or retail superannuation fund, there may be a point in time to accept that you are not using the ‘additional’ features an SMSF can provide.

Therefore, it may be appropriate to wind-up your SMSF and rollover your superannuation to an industry or retail fund.

[1] ASIC: INFO 206 – Advice on self-managed superannuation funds: Disclosure of costs.

Andrew Zbik

Senior Financial Adviser

Creation Wealth

0422 038 253

andrew.zbik@creationwealth.com.au

www.creationwealth.com.au