A good Financial Adviser will devise a strategy that will protect you when you need help. Personal insurances recommended correctly will protect your most valuable asset – you and your ability to earn an income.

A good Financial Adviser will devise a strategy that will protect you when you need help. Personal insurances recommended correctly will protect your most valuable asset – you and your ability to earn an income.

In the past month, I helped a long-standing client to claim on a trauma (also known as critical illness) policy. My client is in their mid-40s, married with two children was diagnosed with cancer. Thankfully, the protection strategy we put in place with insurance has provided a tax-free lump sum payment. My client is now in the position to choose whether they will work or not over the next twelve months whilst receiving medical treatment. They will not have to worry about medical bills as the insurance payout means that they can choose the best treatment they want, upfront, when they need it. This was a six-figure payout … and it doesn’t start with a number ‘1’ or ‘2’.

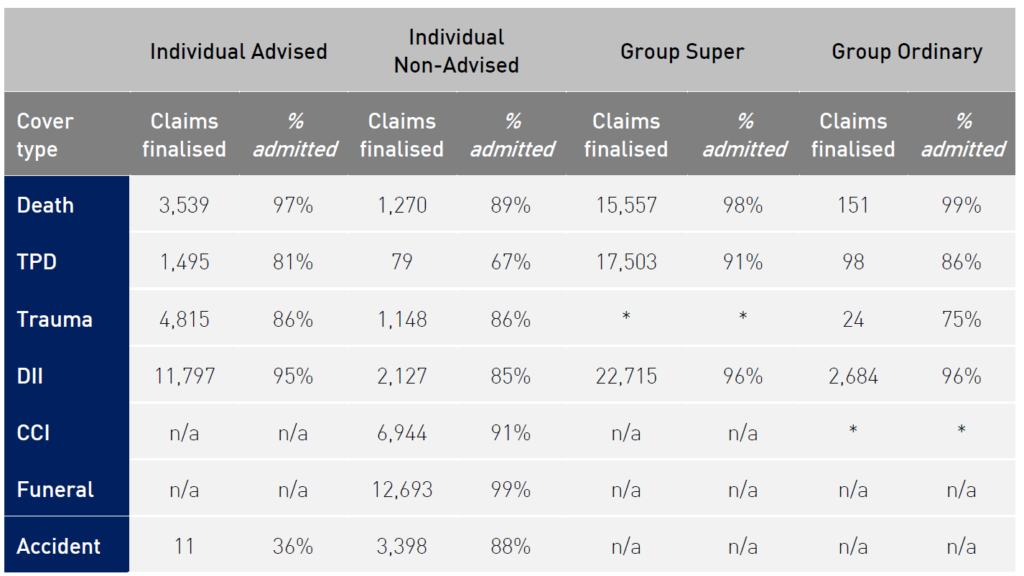

I came across the below table in a report by ASIC which reviews insurance industry claims in Australia. Broadly speaking, people who have obtained an insurance policy through a Financial Adviser or Group Super Scheme (i.e. employer sponsored fund or industry super fund) benefit from a higher percentage of successfully paid claims compared to people who try to go it alone. This is particularly noticeable for Life Insurance, total and permanent disability insurance and disability income or income protection insurance.

For statistical reasoning, it is important to note ASIC notes that some caution needs to be taken when interpreting these results, as some categories have a very low base with which to compare.

Claims admittance rate by cover type and distribution channel

Note: DII = Disability Income Insurance or Income Protection. CCI = Consumer Credit Insurance

Looking at the results, I think there are various reasons as to why there is a significant variance between those who seek insurance advice and those who do not.

1. More total and permanent disability claims via Advisers and Group Super

When I speak with many clients, there is a very low awareness as to what total and permanent disability insurance is. ASIC Moneysmart explains that Total and permanent disability (TPD) insurance provides cover if you are totally and permanently disabled. It helps cover the costs of rehabilitation, debt repayments and the future cost of living.

Your insurer will define TPD as either when you:

- cannot work again in any occupation, or

- cannot work in your usual occupation.

There is a lack of awareness amongst those who go it alone that this type of insurance even exists. I think that is reflected in the very low number of claims (79) for those who went it alone versus the 18,998 who went via an Adviser or Group Super scheme.

2. More disability income/income protection claims via Advisers and Group Super

This type of insurance cover replaces the income lost through inability to work due to injury or sickness. There are many levers which can change how you may benefit from this type of insurance.

For example, the waiting period (the amount of time since your injury or illness until you can lodge a claim) can vary from 14, 30, 60, 90, 180 days to 1 to 2 years.

The benefit period (how long the benefit will be paid) can vary from 2 years, 5 years, to age 65 and now even age 70.

How you set up your income protection insurance will heavily influence how and when you can make a claim.

3. When in need, you have someone to call if you received advice from an Adviser or Group Super scheme.

When my client was diagnosed with cancer, they called me. I was able to do all the groundwork for investigating whether they were able to make a claim and then helped them through the claims process. It took 49 days from when my client informed me that they had cancer to when they received their benefit payout.

Insurance is a complex thing. Different insurance policies cover you for different events. The right combination of insurance complement each other to give you protection for several different scenarios which may stop you from working. A Financial Adviser ensures you have the right insurance in the first place, reviews your policies annually to ensure they are still right for you and is available for you when you need help – especially when a claim needs to be made.

Source (published): ASIC, Statistics Life Insurance Claims and Disputes Statistics, December 2019 (released 21 April 2020)

Notes on ASIC table:

Table 4 summarises the claims admittance rate by cover type and distribution channel. While only Group Ordinary CCI is masked, several other combinations have a very small number of claims finalised in the reporting period: Individual Advised Accident (11 claims across the industry), Individual Non-Advised TPD (79 claims], Group Ordinary Death (151 claims), Group Ordinary TPD (98 claims) and Group Ordinary Trauma (24 claims). APRA urges caution in interpreting the results for these combinations, as such a low volume of claims leads to more volatility in the reported admittance rates.

Andrew Zbik

Senior Financial Planner

Creation Wealth

0422 038 253

andrew.zbik@creationwealth.com.au

www.creationwealth.com.au