Over the last week conversations have continued with my clients about the recent share market drop. Several clients have asked what role Exchange Traded Funds (ETFs) have played?

There are some commentators out there stating that the index approached used by ETFs are stifling liquidity, the underlying assets fluctuate in value (just like direct shares do) and that the passive index approach means you are buying bad performers propping up their share price where they should otherwise be allowed to fail.

My take on ETFs are they are not to blame for any market movements as they are no different to any other way investors can participate in the share market.

Big growth in Exchange Traded Funds

The first ETF was listed in Canada in 1990. In that time the growth in the ETF market has been massive. However, despite the attention, ETFs still make up a relatively small portion of the share market.

According to a report by the RBA last year, ETF’s share of the Australian market is under 2% of the local share market total value. In comparison, ETFs make up around 5% of the share market in Canada and Europe and 10% in the USA.

In all of these shares markets, ownership by fund managers and households is still larger than the proportion of the market owned through ETFs.

Why the massive growth in the use of ETFs?

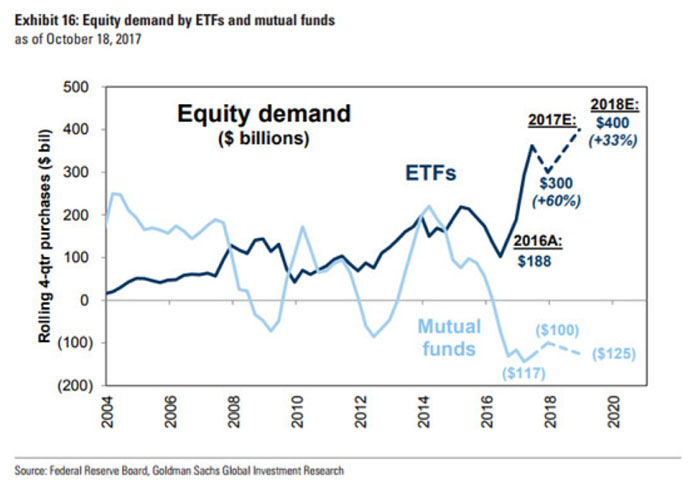

The trend for investors preferring ETFs now over mutual funds (aka managed funds) is clear. Goldman Sachs has produced the below forecast that shows the expected inflows of investor money into ETFs is only going to continue.

So why is the demand for ETFs growing at such a strong pace?

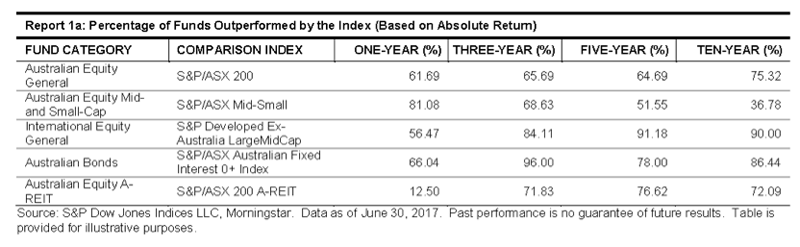

I think it is abundantly clear now that the old approach of trying to pick individual share winners does not work. We now have over ten years of data in Australia alone that shows active fund managers do not beat the general market. That is, a fund manager may look at the top 200 companies on the stock exchange and try and pick the top 40 companies that they think will perform well.

Comparing their stock picking ability to just buying the top 200 companies according to their market value shows that after one, three, five and ten years, just buying the top 200 companies provides a better result. The one exception to this is small cap managers.

These are the fund managers who look at all the small companies listed on the stock exchange that you and I have probably never heard of. As you can see below, small cap managers can outperform their sector of the market over the long-term.

Tackling the claims that ETFs are troublesome

As mentioned, there are plenty of market commentators out there trying to fight the trend investor money gaining share market exposure through ETFs. Here are a few rebuttals I have:

ETFs aren’t buying something real

This is somewhat true but to use it as a general argument is misleading. Broadly speaking, there are two types of ETFs – synthetic and physical. Synthetic ETFs will provide an exposure to a particular asset but not actually own it. For example, there are many ETFs on the market that will enable to you to purchase a commodity such as gold, oil or coal.

When you buy an oil ETF, you are not actually buying barrels of oil but oil futures. So yes, these type of ETFs are not buying the real thing but a fancy financial instrument that is linked to the performance of a particular asset. In general, I have steered clear of these ETFs for my clients.

Then there are physical ETFs. These are the ETFs that will actually go and purchase an underlying real asset. For example, one of the ETFs I recommend to my clients provides an exposure to the ASX200 (or the top 200 companies on the Australian market).

The manager of this ETF will then go and actually buy the top 200 companies on the market. They companies pay dividends and these flow through to the ETF manager and are then paid to ETF owners. A true case of owning a basket of shares. I always recommend my clients invest in ETFs that own the physical underlying asset.

ETFs are stifling market liquidity

I’ve read articles that argue that if everyone buys ETFs and uses the passive investment approach, how will the share market then decide the price of shares based on investors willing to buy and sell? Well if 100% of the market was owed thought ETF’s and no one was allowed to add or subtract to their share market investments this argument may have a case.

However, as mentioned before, ETFs account for under 2% of the Australian market. Plus, as a market as a whole there is always investor money entering a leaving the market (i.e. using cash savings to buy into the market), there is genuine merger and acquisition activity when companies decide to take over another company or split their operations into two separate entities.

There are direct shareholders who were either founders of the company are employees who have earned shares through employer share schemes. Then there are the examples of the companies that perform exceptionally well and investors want to own more of, or companies that fail and become worthless.

For all of these reasons, it is clear that ETFs cannot be held responsible for the claim that they stifle market liquidity. If you want to argue that ETFs stop the market from backing winners and pulling support away from losers – please refer to my earlier comments about the performance of active managers versus the passive approach over the long-term.

Management fees may be cheaper but brokerage costs can be higher

Some commentators have argued that although ETF management fees are generally cheaper that managed funds, the costs of brokerage can be higher. This may be somewhat true for really small holdings in ETFs say under $5,000.

However, many fund managers will charge what is called a ‘spread’ on buying or selling units in a particular managed fund. For example, to buy a unit in a managed fund may cost $0.99 per unit and to sell will earn you back $0.98 per unit. In effect, a brokerage fee. Like any investment decision, the costs must be weighed up against the size of the investment being made.

The underlying assets of the ETF may vary from the price you pay

This is true. But an ordinary portfolio of shares also fluctuates in value. As a rule of thumb, I will never trade an ETF within the first hour of trade or the last hour. The ETF manager needs to provide a market where the price of the ETF matches the value of the underlying basket of assets.

For firms like ours where we will trade in large transactions with ETFs we are aware that we will need to work with the ETF manager to ensure when we transact $3 million in one ETF that we are getting a price that matches the underlying value of the assets in that ETF. Levelling this argument against ETFs is unfair as the exact same problem exists with fund managers.

In summary, I hope some of the queries around ETFs and their role in our market have been clarified. Like any investment, a decision needs to be made in the context of a greater investment strategy and the purpose for your investment activity.

SOURCES:

· https://www.ft.com/content/83b26c8c-d42c-11e7-a303-9060cb1e5f44

· Class SMSF Benchmark Report – December 2017

· Goldman Sachs Sees Big ETF Inflows In 2018

· RBA bulletin (PDF)

Andrew Zbik

Senior Financial Planner

Omniwealth

t: (02) 9112 4316

m: 0422 038 253

andrew.zbik@omniwealth.com.au

www.omniwealth.com.au