The good, the bad and the unintended consequences of 18 years of refunding excess dividend imputation credits.

The debate about dividend imputation credits and how they are dealt with as part of our taxation system looks like it will be here to stay to at least the next Federal election.

A quick history lesson. Dividend imputation credits were something that was introduced back in the days of the Hawke/Keating Government in 1987. In essence, the dividend imputation credit system ensures an investor does not see their income from their investments ‘double taxed’. A company pays tax on its profits and investors pay tax again on the dividend based on their marginal tax rate.

For example, if a company earns $1 in profit – 30% or 30 cents is paid in company tax. The investor then earns a 70 cent dividend. If that dividend were taxed at the investor’s marginal tax rate of let’s say 32.5% – another 22.75 cents is paid in tax. On the original gross profit of one dollar – a total of 52.75 cents would be paid in tax or a whopping 52.75%. Imputation credits factor in what company tax has already been paid.

Thus, when the investor earns a 70 cent dividend, the ATO will factor in what tax has already been paid by the company. Thus, as our investor has a higher marginal tax rate (32.5% in this example) than the company tax rate of 30% – they will only need to make up the 2.5% difference.

Where this works in reverse is if you have your assets in superannuation or your personal tax rate is below the company tax rate. For example, every working Australian who has their superannuation in accumulation phase has a tax rate of 15%. Thus, the excess tax that has been paid by the company gets refunded back to you by the ATO.

Prior to 1 July 2000, you could only offset these imputation credits against other gross tax payable in that financial year. If you had more imputation credits than gross tax payable, these were effectively “lost”.

After July 2000 the Howard/Costello Government changed the rules to allow these excess credits to be returned as a cash refund. Yes that’s right – the ATO gives you cash back. This really came into a world of its own when in 2006 superannuation rules changed to allow Australians in retirement phase to pay NO TAX on their pensions from their superannuation funds.

Thus, if you own Australian shares in your superannuation fund and you are drawing a pension any company tax that was paid by a company was refunded to you in full as you had no tax liability. This was a very handsome boost to income.

So what impact has this system of dividend imputation credit had? Well a report from Credit Suisse has found that superannuation funds now own half of the entire Australia stock market. ATO research shows SMSF’s have approximately 46% of their assets allocated to Australian shares and trusts. Compared to only 6.4% allocated to international shares.

There is no doubt in my mind and experience that the dividend imputation credit system has skewed Australian investors to have an overweight allocation to Australia shares. Australian shares are defined as a ‘growth’ asset and are susceptible to greater volatility compared to property and fixed income assets. The chase for yield has been attracting many Australian investors for two decades. But the consequences of a lack of diversification have been demonstrated in the last year.

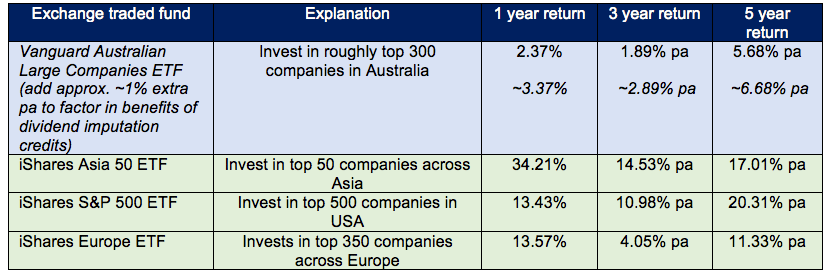

The below table shows what returns Australian investors could have had if they were not purely chasing income yield based on imputation credits:

Over the last three years I have started working with many retirees who came to me with close to 100% of their assets invested in Australian shares to maximise imputation credits. I am glad that I have taught them and advised them to diversify their portfolios across Australian shares, international shares, property, fixed income securities and cash.

So regardless of the outcome on the political debate about how to treat excess dividend imputation credits, Investors should not allow tax policy to drive their asset allocation.

SOURCES:

https://theconversation.com/viewpoints-could-labors-tax-changes-make-the-system-fairer-or-hurt-investors-93280

https://www.businessinsider.com.au/australian-super-funds-now-own-almost-half-of-the-australian-stock-market-2018-3

Andrew Zbik

Senior Financial Planner

Omniwealth

t: (02) 9112 4316

m: 0422 038 253

andrew.zbik@omniwealth.com.au

www.omniwealth.com.au