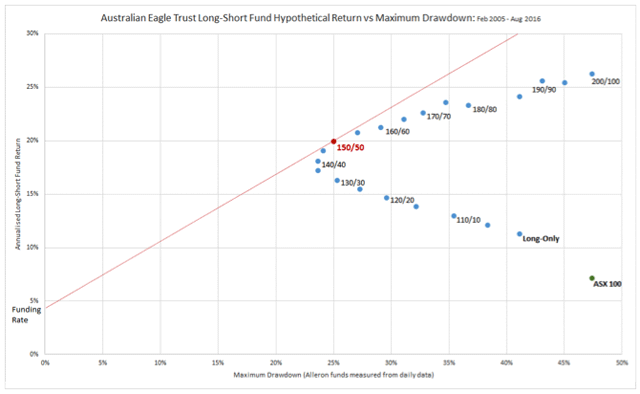

A 150/50 structure can be an efficient solution for extracting the best risk/return from an approach that tends to be long high-quality stocks and short low-quality stocks.

For equities fund manager, Alleron, a 150% geared long portfolio funded by a 50% short sold portfolio, “150/50”, provides a sensible compromise between maximising returns and minimising portfolio risk and, we believe, will deliver a better risk return outcome for investors than a long only portfolio or a market neutral portfolio.

“Market neutral paradoxically can be more exposed to drawdown risk than a 150/50 structure when low quality stocks run hard,” said Barry Littler, CEO, Alleron Investment Management.

Alleron’s investment process identifies stocks with superior quality characteristics, sensible valuation upside and the potential for transformative change backed up by tangible evidence of that change – a “trigger” event in Alleron’s lexicon.

The Australian Eagle Trust Long-Short Fund marries Alleron’s long-only portfolio with a portfolio of shorts of generally poorer quality, overvalued equities. Based on simulations back to 2005, the shorts exhibit a negative alpha correlation to the Alleron long portfolio which assists in improving the risk/return characteristics of the long-short portfolio in falling markets.

For wholesale clients only. Not to be relied on by any other person or seen as advice.

Barry Littler

Chairman/CEO

Alleron Investment Management

North Sydney

barry.littler@alleron.com.au

t: (02) 8252 7559