Portfolio Performance

Portfolio Commentary

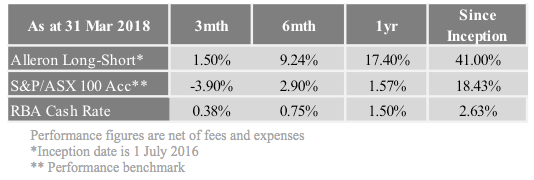

Alleron’s Long Short Fund produced a return of +1.50% for the March 2018 quarter compared to the -3.90% fall in the ASX 100. This is the second quarter since inception the Fund has produced a positive return in a falling market and was also the Fund’s 4th consecutive quarter of outperformance. Net return after fees since inception has now reached +41%, compared to the market return of +18.43% over the same period.

The Australian market fell in the March quarter as international markets experienced increased volatility from trade war tensions between China and the US. The US economy continued to grow strongly with the Fed increasing interest rates by 25bps and the Chairman confirming at least a further 2 hikes in 2018. Subdued Chinese construction activity after the Lunar New Year break resulted in volatility in the iron ore price and other related commodity prices. The big banks were under pressure from constant negative media attention surrounding the Royal Commission into bank misconduct.

The Long side of Alleron’s portfolio performed very strongly, driven, during reporting season, by stocks with earnings growth and positive outlook statements. NextDC upgraded its FY18 outlook from increasing contracted utilisation and operating leverage. Treasury Wine Estates’ Asian growth continued to impress the market while Lovisa’s UK store rollout made strong progress towards its 100 store target. Altium’s strong performance across all regions and product divisions produced an impressive 50% increase in EPS.

The Short side of the portfolio contributed to performance as some stocks missed guidance and reported increasing margin pressure. Short positions in Vocus and TPG Telecom added as both increased debt levels and reported lower profits from significant industry headwinds. Domino’s Pizza downgraded its same store sales guidance for FY18. Short positions in income stocks contributed due to the interest rate hike during the quarter.

Australian Eagle Trust Long Short Fund – Net Monthly Returns

Portfolio Highlights

Positives:

Altium Ltd (Long) – Double digit revenue and profit growth at the HY18 result with strong contributions from China and recent bolt-on acquisitions have shown steady momentum towards their 2020 goal of $200m revenue and 35% EBITDA margins.

Lovisa Holdings Ltd (Long) – The Company’s strong same store sales growth above the company’s own expectations has carried through to the beginning of 2H18, adding to the expansion of pilot stores in new territories in the US and continental Europe.

Cochlear Ltd (Long) – The successful launch of the new Nucleus 7 Sound Processor and a strong performance in developed markets have laid a platform for solid future organic growth. Management reaffirmed FY18 profit guidance at $240-250m.

Negatives:

Coca-Cola Amatil Ltd (Short) – The share price rose despite the FY17 result showing negative growth in the core Australian soft drinks division. The Company expects all other divisions to grow modestly in FY18.

Fortescue Metals Group Ltd (Long) – The share price fell as the lower grade iron ore price discount widened in excess of the Company’s own expectations. Management has been using its strong free cashflow to continue repaying debt to lessen the interest expense burden.

Graincorp Ltd (Short) – The share price rallied despite the Company downgrading FY18 earnings guidance to be 50% below pcp. Significantly lower grain stock from prolonged hot and dry weather has more than offset the US corporate tax rate benefit.

Market Overview

The Australian market fell as US tax cuts were offset by trade war threats and global tech stock sell offs. QBE’s new CEO reset expectations on the existing businesses after selling its Latin America division. With the ongoing AUSTRAC investigation, CBA named its current retail banking boss as new Group CEO. Japara Healthcare acquired 4 aged care facility sites, adding $4m to FY19 EBITDA. Treasury Wine Estates announced a new route to market strategy to increase efficiencies whilst growing its new French wine portfolio in Asia.

Portfolio Changes

Increased Exposure:

Computershare Ltd (+1.50%; New Long): A share registry and business services company. Strong revenue growth and economies of scale in US & UK mortgage services divisions are providing a solid platform for future organic growth.

Sims Metal Management Ltd (+1.50%; New Long): A scrap metals and electronics recycling company. A strong US economic outlook and internal efficiency enhancements have improved the Company’s outlook.

Santos Ltd (+0.75%; Exit Short): A natural gas company. Continual cost cutting and divestment of non-core assets has reduced the Company’s risk profile in an increasingly volatile oil price environment.

Decreased Exposure:

Nanosonics Ltd (-1.85%; Exit Long): A manufacturer and distributor of ultrasound probe disinfectors. The Company’s international growth has shown signs of slowing with negative US growth and sluggish adoption rates in newer territories.

Downer EDI Ltd (-1.00%; Exit Long): A mining services and infrastructure construction company. The Company’s loss of key mining contracts and its takeover of Spotless have decreased potential for earnings growth.

Spark Infrastructure Group Ltd (-2.50%; New Short): An electricity infrastructure provider. The business’s high gearing leaves the dividend vulnerable to a potential rise in interest rates.

Quarter-End Position & Portfolio Exposures

As at 31 March 2018, the fund had a net exposure of 95.49% and gross exposure of 194.68% to equities. Cash was 4.51%.

Major portfolio exposures were to medical devices & services and resource stocks with less portfolio weight in major banks and income stocks.

Stock Highlight

QBE Insurance Group Limited (QBE) – Long Position

Energy Argument: As we have suggested in past reports, part of our competitive advantage is to look back further in a company’s history to determine its potential today. QBE historically were able to roll-up niche insurance businesses where they had some advantage in pricing risk. All of that changed after buying Winterthur in the US. This, along with a change of management seemed to have resulted in a loss of that advantage. Alleron believes that a simplified smaller company provides an opportunity to improve risk outcomes and returns to shareholders.

Trigger: Having spent 3 years as CFO and successfully rectified problems in 2017 as Australia and New Zealand division CEO, Pat Regan was the natural replacement for the outgoing CEO. The new CEO has started his tenure with a methodical approach, reviewing the entire business and subsequently selling its troublesome Latin America division for a $100m profit above book value of $309m. With the new CEO’s indications along with his initial actions, Alleron believes that the company is beginning the process of change that we have been waiting for, opening the opportunity for a change in earnings growth.

Outlook: While the initial trigger to invest in QBE was new management’s focus on simplifying the business, there are a number of potential tailwinds that could also benefit company earnings in the next few years. Firstly, the core underwriting business profitability will be helped by improved insurance premiums after the worst year of natural disasters since Hurricane Katrina in 2005. Secondly, the US Fed expects to raise interest rates a minimum 3 times in 2018, making the $26bn short duration fixed interest investment book a major beneficiary of this interest rate tail wind. With the company trading at under 1.2X book value, Alleron sees minimal downside from here with the opportunity of much larger upside should our Energy argument be confirmed.

Sean Sequeira CFA

CIO

Alleron Investment Management

t: (02) 8252 7563

sean.sequeira@alleron.com.au