Did you know a self-managed super fund (SMSF) can borrow money to purchase assets such as property and shares?

The lending structure used is called a ‘limited recourse borrowing arrangement’ (LRBA).

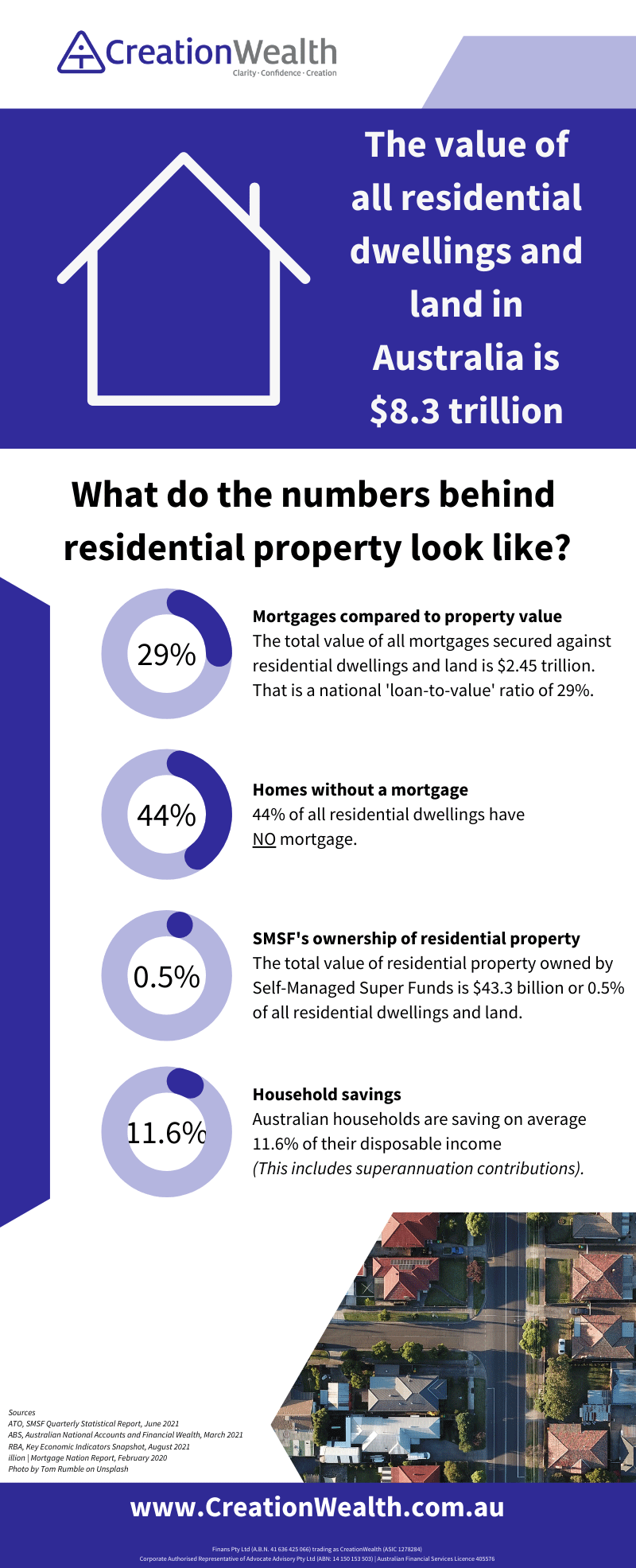

LRBAs have grown substantially since 2007 when SMSFs were permitted for the first time to borrow money to buy assets like property and shares. Putting this into perspective, the total value of residential mortgage loans in Australia today is approximately $2.450 trillion.[i] As at June 2021 total LRBAs in self-managed superannuation funds amounted to just under $57 billion.[ii] Thus, assuming most LRBAs are for the purpose of purchasing property (we don’t actually know from the ATO the split between loans used to buy property and loans used to buy shares), LRBAs within the superannuation system account for 2.32% of all loans.

The current value of the Australian residential property market is approximately $8.3 trillion.[iii] As at June 2021 the value of residential property within SMSFs was approximately $43 billion.[iv] When taking the total value of residential property purchased in SMSFs into perspective, this accounts for only 0.52% of the value of all residential properties in Australia.

The relative value of both LRBAs within the superannuation system is relatively small compared to the value of the Australian financial system.

If you are considering using your superannuation to establish your own self-managed superannuation fund to purchase a residential investment property, here are a few broad guidelines I use when considering if such a strategy is appropriate for my clients.

1. Minimum super balance

The Australian Securities and Investment Commission (ASIC) is of the opinion that a minimum of $500,000 is required to establish an SMSF. However, most lenders are now requiring a 10% liquidity buffer of cash and/or shares outside of the value of the property. The Australian Taxation Office has also highlighted the obligations of SMSF Trustees to consider asset diversification within the fund. Thus, the days of starting an SMSF with a balance of $200,000 to buy an investment property as the sole asset of the fund is no longer deemed to be in the best interest of the members of the fund due to a lack of asset diversification and a lack of liquidity.

Other considerations are if the fund has two members earning an income, would the ability of the SMSF to service the debt be affected if one of the members loses their job? I always base lending capacity on one income only. This helps to preserve cash flow in the unfortunate situation where a member may be out of work for a few months.

2. At least 10 years of working life left

This is not an ideal strategy for people who have less than ten years to work. A full property cycle in Australia is around 10 years. You need to give time for your property to grow in value. Ideally, the intention should be to hold the property beyond this minimum time period of 10 years. Once a superannuation fund owns an investment property, the only time I envisage that the property needs to be sold is when all the debt has been paid off and the sale of the property will allow the net proceeds to be invested into another asset class that provides a higher income yield.

The average gross rental yield for property in Australia currently hovers between 3.5% to 4.5%. A good portfolio of exchange-traded funds (ETFs) and some direct shares can provide a dividend yield of between 3% to 5% with the prospects of capital growth too. A good portfolio of fixed income assets such as bonds can provide a stable income of between 2% to 4% but with limited capital growth prospects.

Thus, I believe property is a great asset to provide leverage and capital growth, but property is not necessarily the best income-producing asset to provide an income stream to fund an account-based pension. With property, it is not possible to shave off a bedroom and sell it to provide cash for pensions.

3. Protect your cash flow

What happens if one of the members loses their job? Or if you lose a tenant? I always recommend that an SMSF hold a cash buffer that amounts to six-months of all property expenses which includes loan repayments and rental costs such as landlord insurance, strata fees and council rates. This additional cash buffer may be held in an offset account against the superannuation fund loan. That way you are helping to reduce your lending expenses via the rate of interest paid. It also helps to improve the cash flow of the fund. A good diversification strategy would also include other liquid assets such as Australian shares, international shares and fixed-income securities. In a worst-case scenario, if the members of the fund are not working for a period longer than six months, there are other assets available to liquidate without relying on a ‘fire sale’ of the property.

4. What is your plan to pay off the loan?

Whenever you take on a loan, you need a plan to pay down this loan. Will your concessional contributions be enough to pay out the loan? Will you need to make extra contributions to your SMSF to have the property loan paid down before retirement? These questions need to be answered.

Most people are only receiving the statutory superannuation guarantee of 10%. I never rely on a debt reduction plan that involves selling the asset itself. This is actually against best practice when obtaining credit. I like it when clients have the ability to make additional superannuation contributions to the fund or have other assets in the fund outside of the property (such as shares or ETFs) that produce income and capital growth. This additional cash flow, capital growth and income can be used to reduce the debt without relying on the sale of the property itself.

[i] ABS, Australian National Accounts and Financial Wealth, March 2021

[ii] ATO, SMSF Quarterly Statistical Report, June 2021

[iii] ABS, Australian National Accounts and Financial Wealth, March 2021

[iv] ATO, SMSF Quarterly Statistical Report, June 2021

Andrew Zbik

Senior Financial Adviser

Creation Wealth

0422 038 253

andrew.zbik@creationwealth.com.au