Hugh Dive, Senior Portfolio Manager with Aurora Funds Management, makes the case for short selling.

The financial press frequently paints the picture of hidden cabals of short sellers conspiring together to drive down a stock, causing unrealised losses to retail investors and pain to executives whose company’s stock have been sold short. Whilst short-sellers are frequently derided as vultures, criminals, pessimists or un-Australian, in reality shorting stocks is a hard, stressful and lonely way to make money in the market. Short selling allows an investor to profit from taking a contrarian view.

How it works

Unlike long only investing where you seek to own good quality companies with honest management teams, clean balance sheets and solid future prospects, when selecting a stock to short sell the characteristics to look for are companies with low or negative growth, high and increasing debt levels, a weak business model, over-valued by a market and possessing a shaky management team. Short sellers will then borrow stock from a stockbroker and sell it, essentially betting that the price of the target company will decline before they have to replace the borrowed shares by buying the stock back. The short seller is both required to return the shares to the owner when requested and pass on any dividends paid.

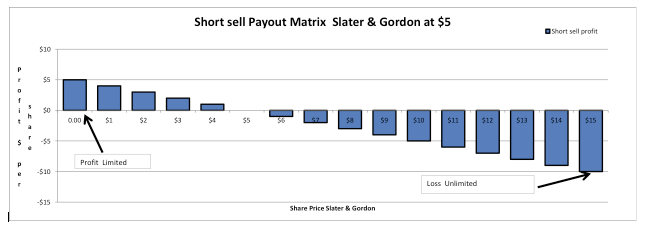

Additionally if the short stock rises sharply, the lender may require additional collateral or require the short seller to close out your short sale transaction before your planned timeframe. This gives rise to the skewed payoff ratio from short selling where the maximum gain is known (the stock falls to zero), but the maximum loss is theoretically infinite. See below chart on the payoff matrix we faced when shorting Slater & Gordon (SGH) at $5.

When borrowing shares to short sell an investor has to look closely at both the rate per annum that they are required to pay to borrow the stock and where the owner is located geographically. The rate reflects supply and demand and for most stocks is currently 0.5% per annum. For stocks where the shorting demand may be higher than the supply such as Fortescue the rate may be 15% or higher, or in the case of small capitalisation or tightly held companies such as Blackmores, the short seller may be unable to borrow stock and thus cannot short sell.

We also strongly prefer to borrow stock from foreign owners such as large index funds like Vanguard or State Street, as if we borrow stock from a domestic owner and a dividend is paid we are required to compensate for both the dividend and any associated franking credits.

For example in July 2015, we shorted Slater & Gordon at $3.70 per share, paid the lender the rate of 0.5% per annum and then bought the stock back at $1 to close out the position in December 2015. Whilst the stock has continued to fall in 2016 and our profit would have been greater had we held onto the stock; we were concerned in December that the bulk of the gains in shorting the stock had already been made.

Bans on Short Selling

In September 2008 during the GFC, financial regulators worldwide moved to ban short-selling on financial stocks (such as Westpac and QBE Insurance). This occurred as short-selling of financial stocks globally had dramatically increased due to investor concern about the underlying stability and solvency of many financial institutions after the U.S. government takeover of the housing finance corporations Fannie Mae and Freddie Mac and the failure of investment bank Bear Sterns earlier in March 2008. The objective of the ban was to enable a more orderly functioning of the financial markets and to avoid extreme share price movements and in Australia this ban lasted until the end of May 2009.

However a review by ASIC in 2012 concluded that the ban actually reduced trading activity of Australian stocks; increased bid-ask spreads; reduced liquidity; increased price volatility; and contributed to a decline in the number of settlement failures. Additionally, ASIC were unable to establish a causal relationship between the measures and stock prices. Whilst these moves were initially lauded in the press, they were insufficient to prevent the demise of highly levered companies with unsound business models such as Centro and Babcock & Brown, as ultimately the selling pressure returned even with the bans.

The Market can remain wrong longer than you can remain solvent

It would be wrong to view that short selling risky stocks is a smooth path to outperformance. The father of modern macroeconomics Keynes once famously said that “markets can remain irrational a lot longer than you and I can remain solvent’’. This quote particularly resonated with me after an unprofitable short selling of Fortescue prior to the GFC due to concerns about the over-valuation and debt situation of the company. This trade was put on at $50 per share late 2007 and then was closed out at $70 four months later as the price continued to rise with no signs of slowing momentum. It was very painful to lose 29% in a short stretch of time; however Fortescue peaked at $120 in June 2008 before falling back to $20 in December 2008. Whilst our investment thesis was ultimately correct, we were unable to handle the pain of a steeply rising stock and the associated losses and increasing margin calls.

A “short squeeze” occurs when a heavily shorted stock rises sharply, forcing sellers to close out their position by buying back stock, thus causing further upward price momentum. Often when the market appears to overreact to a small piece of positive news, this is a short squeeze and it is similar to too many people trying to fit through a door. It is conceivable that the impact of many short sellers closing out their positions in Fortescue around early 2008 contributed to a “short squeeze” in the stock and pushed the company’s share price even higher.

Our Thoughts

While short selling is often criticized and retains a negative connotation in a securities industry that is inherently biased towards being optimistic, we see that it serves a valid role in financial markets. Short sellers provide an alternative view and can aid both liquidity and price discovery in stock markets.

Hugh Dive

Senior Portfolio Manager

Aurora Funds Management

0409 443 999

hdive[at]aurorafunds.com.au

www.aurorafunds.com.au