Does it make sense to make additional concessional contributions to superannuation if you still have non-deductible debt such as a home loan?

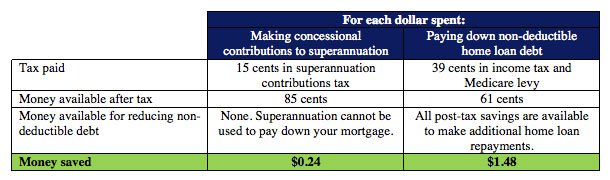

The maths is simple for an average couple on the average tax rate. If $1 of earned income is paid to their personal bank account, the tax man currently collects 39 cents in income tax and Medicare levy. That leaves 61 cents in their pocket.

If they were to make concessional contributions to their super via salary sacrifice arrangement, the tax rate is only 15% on those contributions. Thus, the tax man gets 15 cents and they get to keep 85 cents in their superannuation fund to help build wealth for retirement. A good tax saving of 24 cents or 24% for this example.

For many people it makes more sense to focus on paying down a home loan before making additional contributions to superannuation.

However, this will depend on your marginal tax rate, age and outstanding home loan balance. A good financial planner who focuses on strategy will be able to help you determine the most appropriate path for you to choose.

Source: AWOTE ATO June Quarter 2016

Andrew Zbik

Senior Financial Planner

Omniwealth

t: (02) 9112 4316

m: 0422 038 253

andrew.zbik@omniwealth.com.au

www.omniwealth.com.au